Nuclear Energy: The Deep Dive

The full breakdown on the most promising energy trade of the next decade.

It all starts with a rock called pitchblende.

It’s dense, dark, and largely forgettable, except for one fact: gram for gram, it holds more usable energy than anything else on Earth.

The first step is pulling it out of the ground in Utah, Wyoming, the Athabasca Basin, or the steppes of Kazakhstan. Then, you truck it to a mill. Strip the rare earths and impurities away. Send the newly produced yellowcake to a conversion plant, then to a centrifuge for purification, and finally to a fabricator who packs it into ceramic pellets and stacks them into twelve-foot zirconium rods ready for energy production.

Those rods get loaded into a reactor. Water boils, spinning a generator. Electricity moves at close to the speed of light through the power grid until it arrives where it’s needed — an Anthropic research lab, a Los Angeles suburb, a Texas refinery, or a naval submarine.

Meanwhile, capital runs in reverse.

As electricity and fuel flow up the stack, dollars flow down. Hyperscalers — Microsoft, Amazon, Google, Meta — are signing 15-to-20-year PPAs (power purchase agreements) at price points that would have been unthinkable five years ago. Those dollars cascade through the system: to the utility, to the reactor operator, to the fuel fabricator, to the enricher, to the converter, to the miller, and finally to the companies pulling the ores out of the ground.

This is the full-stack nuclear buildout. And it is the most promising energy trade of the next decade — underwritten in ink, for the next twenty years, by the four largest balance sheets on the planet.

Today, I’m breaking it down layer by layer. Every opportunity. Every name worth owning.

0. The Nuclear Renaissance

For most of the last thirty years, nuclear energy was understood to be a dead technology.

That sentence sounds like an exaggeration. It is not.

After the partial meltdown at Three Mile Island in 1979 and the catastrophe at Chernobyl in 1986, public opinion across most Western countries turned decisively against nuclear power. New construction effectively stopped in the United States. Germany committed to shutting down its entire fleet. Japan idled most of its reactors after the 2011 disaster at Fukushima.

The capital markets followed public mood. By the late 2010s, mines were closing, processing plants were idling, the workforce was aging out, and the few new reactors being built in the West were spectacularly over budget and behind schedule. Demand was almost completely destroyed.

Then, sometime in 2024, everything changed.

The trigger? AI.

Frontier AI models — the systems behind ChatGPT, Claude, Gemini, and the next wave of wrappers and applied products being built on top of them — require staggering amounts of electricity to train. A single training run for a state-of-the-art model can consume as much power as a small city for months on end.

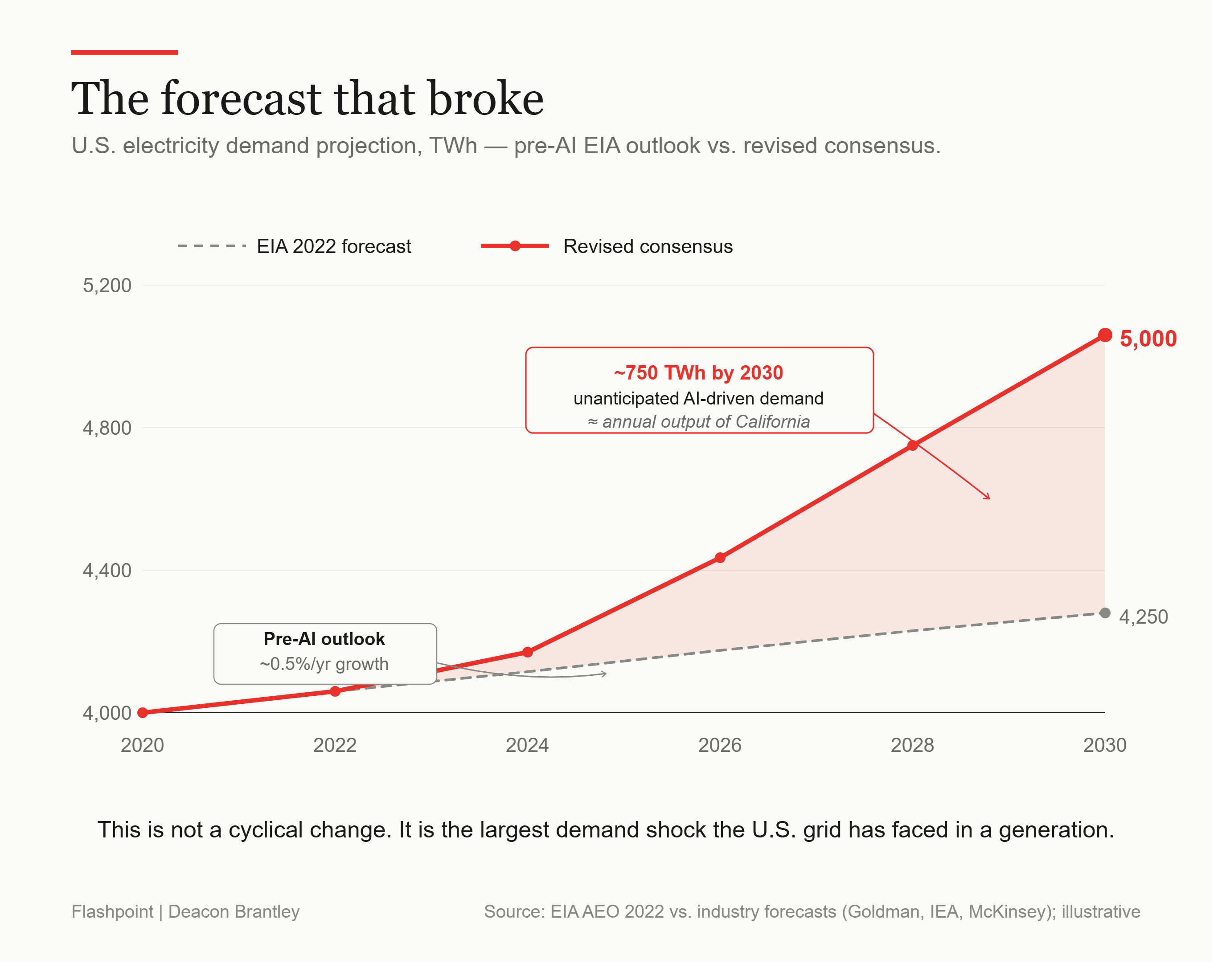

And the federal government’s own electricity demand forecasts from 2022 — the official projections for how much power the country would need in 2030 — are already wildly out of date. The numbers are not off by ten or twenty percent. They are off by entire gigawatts. Multiple New York Cities worth of power.

And the AI buildout has a problem. It’s not just the AI models that need power. It’s the data centers, the chip-making facilities, the assemblers, the campuses. Power demand is accelerating faster than power generation. In a sector where a month-long delay can be the difference between winning the race and losing it, the hyperscalers can’t afford for the legacy American power grid to catch up. And even worse, the current grid can’t.

The overwhelming majority of American power comes from fossil fuels, specifically natural gas. For the power demands of 2030 to be met, fossil fuel production would have to scale exponentially. But pending miraculous new gas field discoveries, this can’t happen.

Renewables aren’t an option either. They’re land-intensive and aren’t reliable enough for the demands of a data center or a chipmaking facility.

There is exactly one technology that produces large amounts of electricity, around the clock, that can scale to the extreme demands of tomorrow. Nuclear. It is the only one. The math leaves no other answer.

The policy layer, in a rare moment of bipartisan clarity, has aligned around this fact. A 2024 law called the ADVANCE Act, which passed the Senate eighty-eight to two, streamlined the process of approving new reactors. The Inflation Reduction Act of 2022 created a federal subsidy for existing nuclear plants. The Department of Energy now has tens of billions of dollars available to lend to nuclear projects. And in May of 2024, the United States banned the import of enriched uranium from Russia, slamming the door on roughly a quarter of the country’s nuclear fuel supply and forcing a domestic rebuild from a depleted starting position (more on that later; sections 8 and 9).

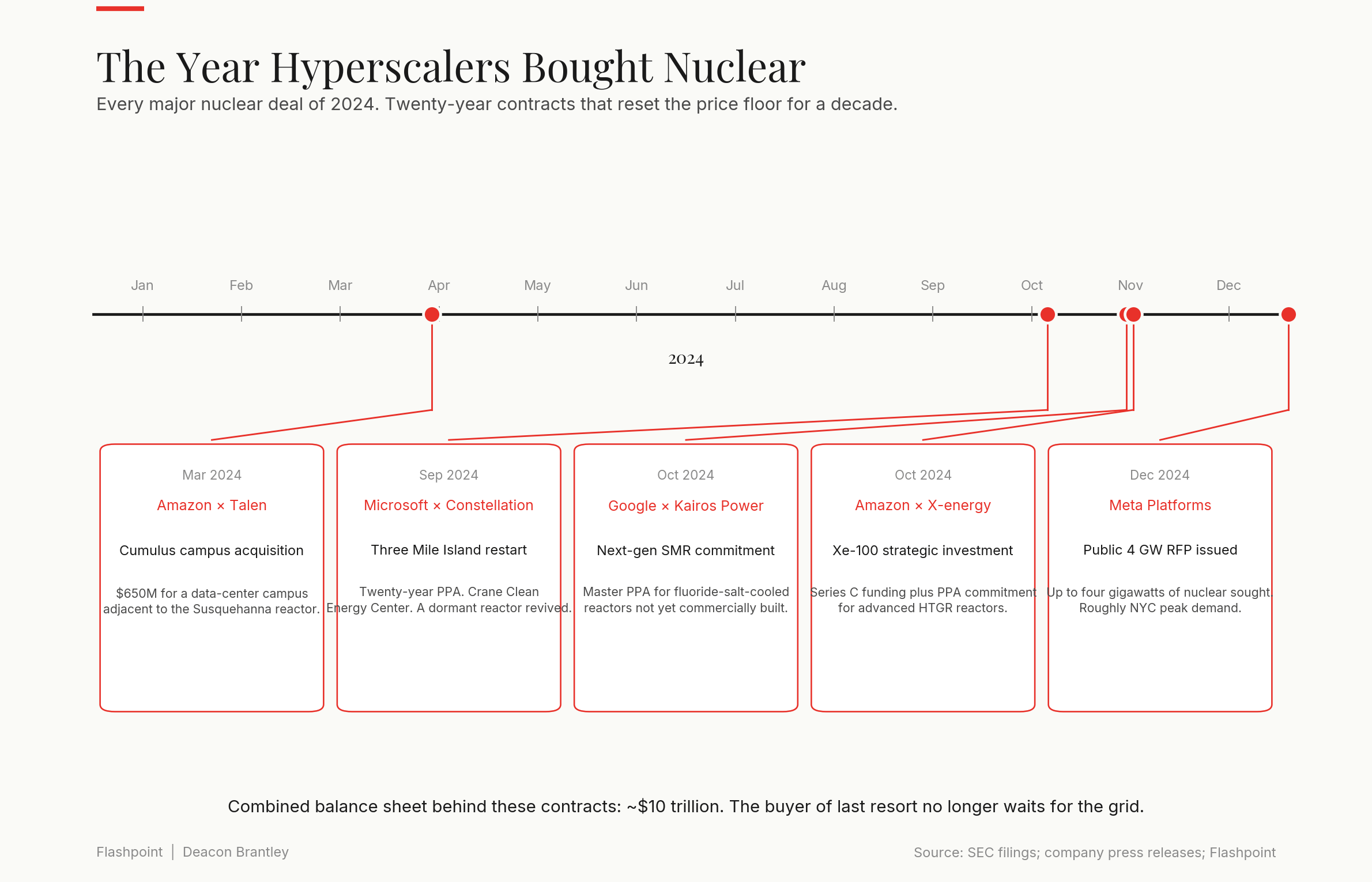

The capital layer moved with it. Microsoft committed to restarting the long-closed Three Mile Island reactor. Amazon paid hundreds of millions of dollars for a data center campus that plugs directly into a nuclear plant. Google signed for next-generation reactors that have not yet been built. Meta issued a public solicitation for up to four gigawatts of nuclear capacity. A handful of startups developing new reactor designs raised billions of dollars at valuations that seemed like pipe dreams only two years earlier (ahem, NuScale).

For over thirty years, every link in the nuclear supply chain had been allowed to atrophy. Mines and conversion facilities were closed. Enrichment and production was outsourced to Russia. Reactor construction projects were suspended or canceled. Today, the entire chain is being asked to scale at once, with demand contracts locked in for twenty years.

This is the story of how there’s suddenly enormous demand for something that almost nobody has been making. That gap — between what the world now needs and what the world is currently capable of producing — is the story of everything that follows.

And it’s why nuclear may be one of the trades of the next decade.

1. The Hyperscalers

Let’s start at the top of the chain.

The four companies that have effectively decided the future of nuclear power are Microsoft, Amazon, Google, and Meta. Their combined value on the stock market is north of ten trillion dollars. Their combined annual profit is approaching two hundred billion. The capital available to them is essentially limitless.

These companies are not trying to enter the nuclear business. They do not want to build reactors. They do not want to mine uranium. They want exactly one thing: a reliable, decades-long supply of electricity. And they are willing to pay almost any price to get it.

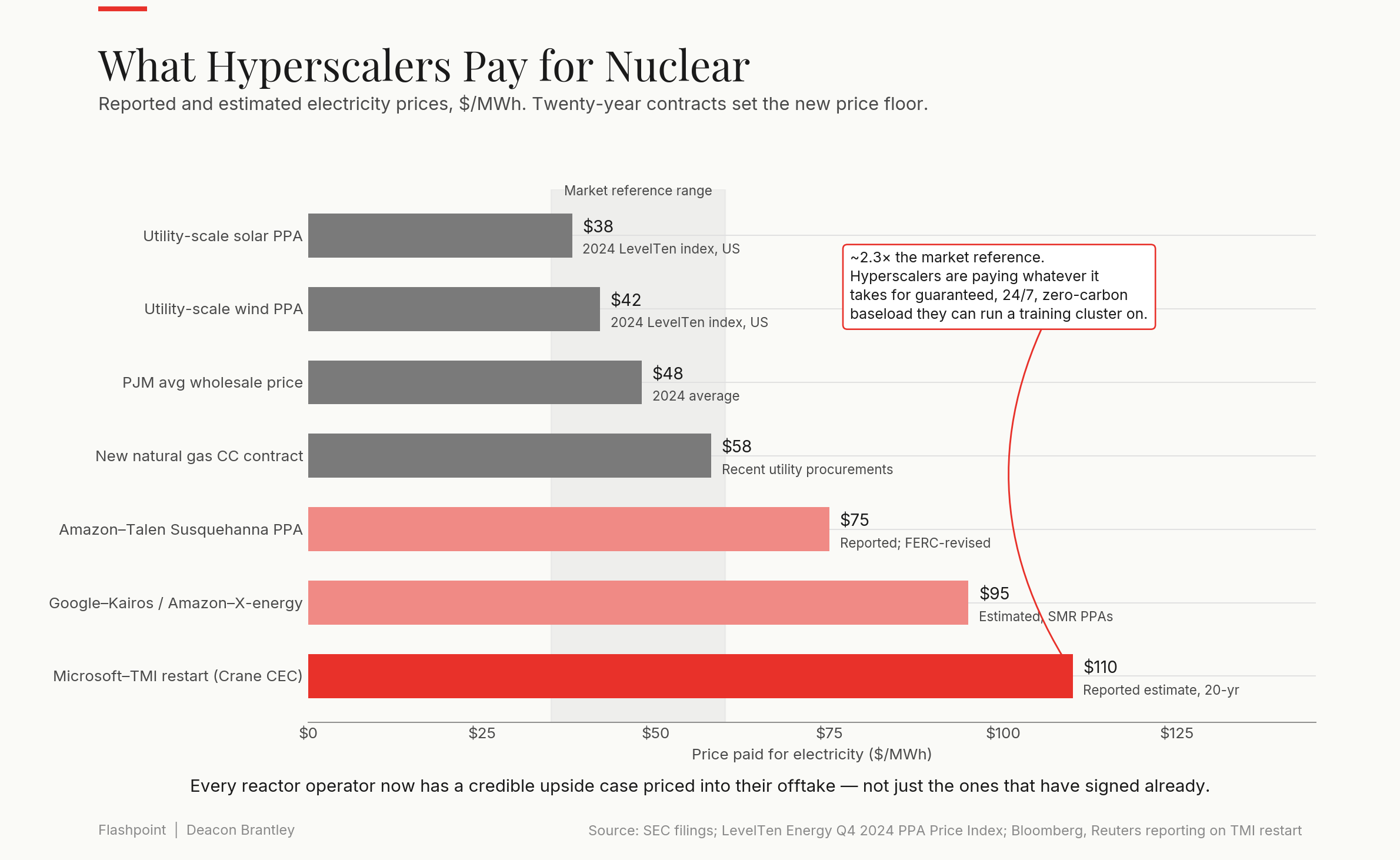

In September of 2024, Microsoft signed a twenty-year contract with the operator of the dormant Three Mile Island plant in Pennsylvania — yes, that Three Mile Island — to bring it back online. The price per kilowatt-hour was never publicly disclosed, but multiple industry sources reported it as well above what any nearby utility was paying for ordinary electricity from a coal or gas plant.

A few months earlier, Amazon had quietly bought a data center campus in Pennsylvania for 650 million dollars. The campus had one notable feature: it sat directly next to an operating nuclear plant called Susquehanna, and could draw its electricity straight from the reactor without ever touching the public power grid.

Google followed with a commitment to buy power from a startup called Kairos that is developing a new generation of smaller, faster-to-build reactors that don’t yet exist commercially. Amazon made a similar bet on a similar company called X-energy (not affiliated with Elon Musk). Meta, late in 2024, issued a public request for proposals for up to four gigawatts of nuclear capacity. Four gigawatts is roughly the peak electricity demand of New York City.

The reframe is important. These four companies are not behaving like customers. They are behaving like generous financial backers willing to provide the lucrative, long-term, guaranteed revenue streams that the rest of the supply chain needs in order to invest in capacity. Their twenty-year contracts have set the floor price for nuclear electricity over the next two decades.

Every other layer of this story — every utility, every mine, every fuel processor — is acting in response to the hyperscalers.

Names worth knowing:

Microsoft ($MSFT), Alphabet ($GOOGL), Amazon ($AMZN), Meta ($META). They aren’t the trade; they’re supplying the capital that justifies every layer below.

2. The Operators

The first layer below the hyperscalers is the plants that already exist — and the corporations operating them.

The United States has roughly 90 active commercial reactors that produce about a fifth of American electricity. For most of the past two decades, these reactors were locked in place. They were too expensive to compete with cheap shale gas, too politically toxic to expand, and just profitable enough to keep running. Several of them closed for purely economic reasons. Vermont Yankee shut down in 2014. Three Mile Island’s Unit 1 shut down in 2019. Indian Point, north of New York City, fully shut down in 2021. Palisades, in Michigan, shut down in 2022.

In the last two years, two of those four — Palisades and Three Mile Island — have already been pulled out of retirement. The economics that made them dead assets in 2022 have completely inverted in less than three years. And nuclear plants can’t just be flipped on and off. Restarting one is a monumentally challenging task — multi-year regulatory review, full refurbishment, license amendments, fuel procurement.

The largest operators of the American reactor fleet are the clearest names in this layer. They already own the plants. They already have the licenses and the knowledge. They already know how to run them.

What has changed is the price they can charge for the electricity those plants produce.

Three years ago, the answer was “market rate, more or less.” Today, the answer is whatever Microsoft and Amazon are willing to pay.

The math looks stunning for these operators. A reactor built decades ago at someone else’s expense, with all debts long paid off, suddenly finds itself in a market where a hyperscaler is offering to sign a twenty-year deal at a high premium. The increase in revenue drops almost entirely to the bottom line. There is negligible new capital involved, only the contract being signed and the electricity already flowing.

The big three nuclear plant operators have signed massive PPA deals already and more keep coming. As recently as June 23, 2026, Constellation signed a 15-year PPA with Walmart. The next reactor brought back from the dead is probably not far away.

Names worth knowing:

Constellation Energy ($CEG) — The safest nuclear utility play in public markets. 22 reactors, over 32 GW of nuclear capacity. Down ~26% YTD in 2026 despite the thesis — a multi-year winner pulling back in the AI-utility rotation. The 3-year return is still above 200%.

Vistra ($VST) — Acquired Energy Harbor’s nuclear fleet in 2024. Comanche Peak in Texas, plus deregulated reactors in PA and OH.

Talen Energy ($TLN) — Owns Susquehanna. The Amazon deal is the cleanest expression of the colocation trade.

3. The Grid

A reactor that nobody can plug into is a useless reactor. Put another way, you need an outlet to charge your phone.

This is the part of the story that consistently gets blown over, because it does not sound like a nuclear story.

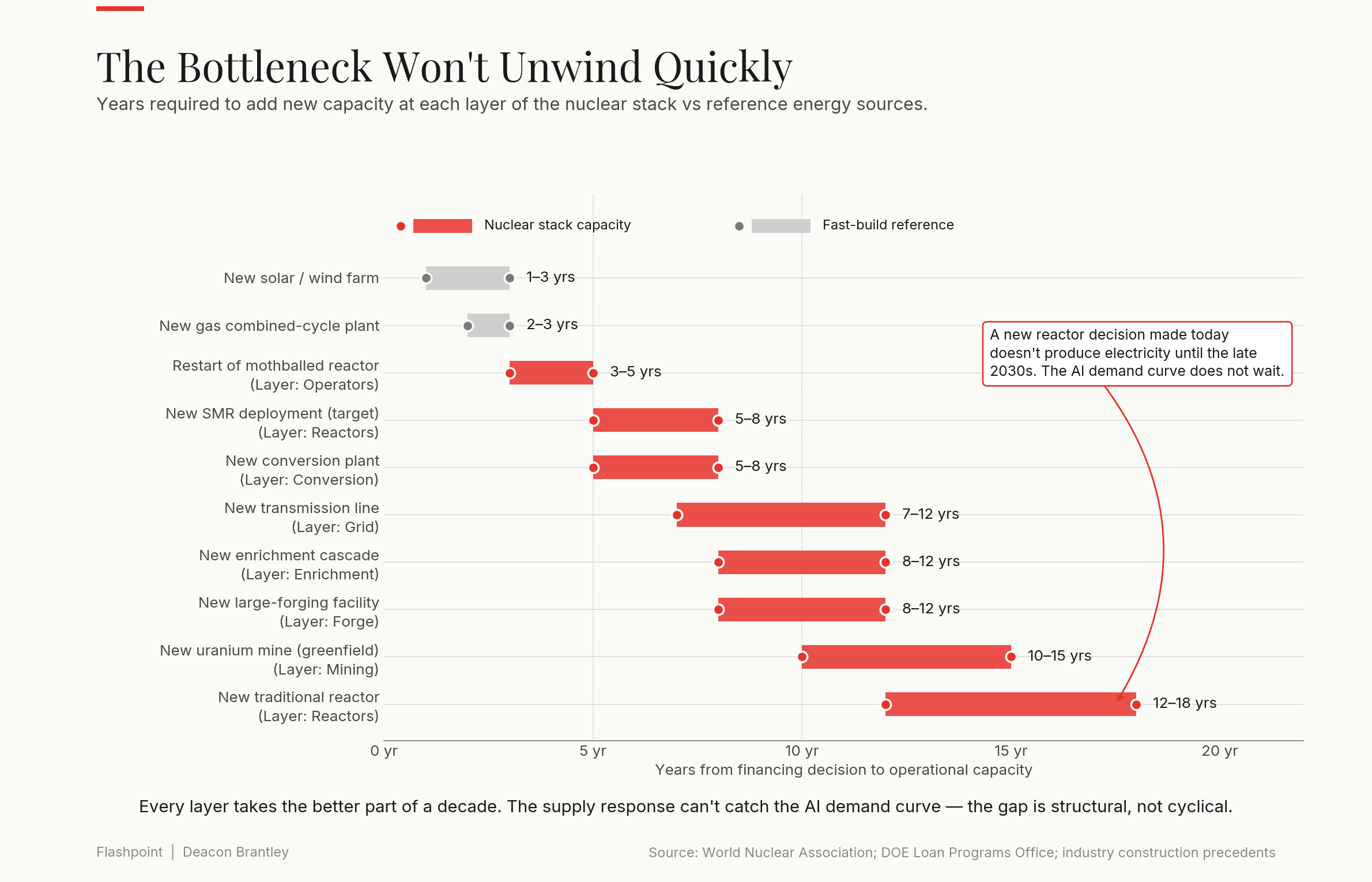

America’s shaky electric grid was built mostly between the 1950s and the 1970s. It was designed for a country that was half the size, drew a fraction of today’s electricity, and did not have to handle the massive concentrated loads that modern data centers represent. New transmission lines — the high-voltage cables that carry electricity from where it is made to where it is consumed — can take a decade to permit and another five years to build. New transformers, the refrigerator-sized devices that step electricity up and down between voltage levels, are back-ordered by years, and the companies that produce them are scrambling to scale. The skilled labor base that can construct transmission infrastructure has been hollowed out by three decades of underinvestment.

This means that even when the reactor exists, and even when the technology company wants its power, there may simply be no way to connect them.

Amazon’s Susquehanna deal was structured around exactly this problem. Rather than wait for transmission upgrades that might never come, Amazon built its data center next to the reactor and bypassed the public grid altogether. But you can’t always do that. The surrounding area of a reactor may not be suitable for a data center and vice versa.

This pattern is going to multiply. The hyperscalers can’t afford to wait for America’s power grid to catch up. They must supply capital to build the transportation layer between their data centers and their reactors. And the industrial companies that supply grid hardware are going to find themselves in a multi-year boom, providing the picks and shovels for the entire buildout.

This is one of the layers where the demand growth is most easily quantified and where the supply response is most obviously inadequate.

Names worth knowing:

GE Vernova ($GEV) — Spun out of GE in April 2024. The closest thing to a vertically integrated grid-plus-generation pure-play. Up 63% YTD in 2026.

Eaton ($ETN) — Power management at every scale, from the data center rack to the utility substation.

Forgent Power Solutions ($FPS) — Electrical distribution equipment for data centers and grid infrastructure. Smaller cap, higher beta. Up over 102% YTD.

Quanta Services ($PWR) — Builds the actual transmission lines. The picks-and-shovels of the picks-and-shovels.

4. The Reactors

Here is the conundrum.

Nuclear works and the technology is mature. We’ve been generating electricity from controlled nuclear reactions since 1954. The reactors themselves, when you look past the political controversy, are among the most reliable machines ever built. The American fleet runs at an average capacity factor of about 92% — meaning the reactors generate at full power for roughly 92% of the hours in a year across a multi-decade lifespan.

The problem is that we no longer know how to build new ones.

The most recent two reactors to come online in the United States are called Vogtle 3 and Vogtle 4, in Georgia. They started construction in 2009. They came online in 2023 and 2024. They were originally budgeted at $14 billion. They cost $35 billion.

That single metric is why the capital flowing into this story is not flowing into more mega-reactors of the same kind. The economics do not work. The construction timelines do not match the demand. By the time a traditional reactor designed today is producing electricity, the AI buildout will already be a decade past.

Two responses are emerging, and this is one of the most exciting parts of the stack.

The first is to make reactors smaller and standardized. This is the concept behind what the industry calls small modular reactors (SMRs) — units that can be manufactured in a factory like aircraft engines, shipped to site, and installed in a fraction of the time a traditional reactor requires. A handful of companies are racing to commercialize designs along these lines. None of them have built or shipped one yet. The leading American name, NuScale (read my deep dive here), has the only design currently certified by federal regulators but has not yet fully built a commercial unit. Others, like Oklo and X-energy, are earlier still.

The bet on any of these companies is not really a bet on nuclear power. It is a bet on whether they specifically will be the ones to actually manufacture the next generation of reactors at scale, and on the regulatory and engineering milestones still ahead of them.

The second response is to lean on a specific category of company that already knows how to build small, compact reactors.

The Navy operates about ninety nuclear reactors today, between its eleven nuclear aircraft carriers and roughly seventy submarines. The company that builds them, BWX Technologies, has spent decades refining a small-reactor manufacturing process that no other commercial entity in the world possesses. As the commercial market belatedly tries to do what the Navy has been doing routinely for sixty years, BWX finds itself in an extraordinarily strong position. It can just adapt its naval reactor designs for submarines into small, sellable commercial reactors. And it doesn’t need to win the SMR race — it just needs to manufacture for whoever does.

Names worth knowing:

BWX Technologies ($BWXT) — The defensible position. Sole US naval reactor manufacturer, real backlog, real moat, real revenue, growing commercial SMR exposure.

NuScale Power ($SMR) — The only NRC-certified SMR design. Highly speculative. Volatile.

Oklo ($OKLO) — Sam Altman–backed compact fast reactor. Pre-revenue, pre-certification, pure optionality.

NANO Nuclear Energy ($NNE) — Microreactor concepts. Earliest stage, narrative-driven.

5. The Forge

It’s not easy to build a nuclear reactor, no matter how small or modular it is. They require large amounts of specialized components, all capable of withstanding natural disasters, meltdowns, terrorist attacks, and time.

One of these components is steel.

Modern reactor pressure vessels must be forged from enormous ingots of steel that have to be poured and worked while still molten. The metallurgy must be perfect. There are, at any given moment, only a few facilities globally capable of producing a forging of the necessary size and quality.

None of them are currently in the United States.

This is the layer of the supply chain that most clearly shows what thirty years of ignorance looks like. We have, slowly, lost the industrial muscle to make the components our own designers want to use. Some of the capacity exists in Japan. Some in South Korea. Some in France. A small amount is being rebuilt domestically, but the lead times to fully restore it are measured in decades.

Specialty metals are part of the same story. Reactor components require alloys with names like Inconel — metals engineered to withstand temperatures and radiation conditions that would destroy ordinary steel. The companies that make them tend to be specialty manufacturers whose products go into nuclear reactors and high-end aerospace engines and very little else. The nuclear renaissance gives them a second growth driver they did not have ten years ago.

The dynamic at this layer is simple. Lead times measured in years. Capacity that cannot be quickly expanded. A small number of companies controlling capabilities nobody else can replicate.

That is the textbook definition of pricing power, and it is going to assert itself over the next decade in ways the market has not yet absorbed.

As the demand for nuclear power increases, so will the demand for constructing nuclear power. These companies win no matter who gets awarded the contracts.

Names worth knowing:

BWX Technologies ($BWXT) — Doubles as both reactor manufacturer (section 4) and component supplier.

Allegheny Technologies ($ATI) — Inconel, titanium, and zirconium specialty alloys.

Curtiss-Wright ($CW) — Specialty nuclear components, instrumentation, and valves.

6. The Fuel

Now, shifting gears. Onto the rock at the heart of every reactor — the uranium.

The final form of nuclear-grade uranium are small ceramic pellets, each about the size of a pencil eraser, each holding as much energy as a ton of coal.

The companies that turn uranium into actual fuel are a small group. The most important is Westinghouse, the American company that designed the most common Western reactor architecture and supplies fuel for many of the reactors built using its designs.

In 2023, Westinghouse was purchased by a Canadian uranium miner called Cameco and a Canadian investment firm called Brookfield — a transaction that quietly took the most important Western nuclear company out of private equity hands and folded it into two publicly traded vehicles. Owning Cameco today gives exposure to the uranium mine at the bottom of the stack and to nearly half of the dominant Western fuel and reactor business at the top of it. There is no other vertically integrated nuclear company in public markets that comes close.

For the next generation of reactors — the small modular kind — fuel is a different problem entirely. The advanced designs need a more concentrated form of uranium than conventional reactors use — a form that causes lawmakers to raise their eyebrows. The capacity to produce that more concentrated form does not yet exist in the United States at meaningful scale. A single company, called Centrus, headquartered in Maryland with production in Piketon, Ohio, is currently producing it in kilogram quantities, against an eventual need of tens of tons per year.

You can’t run a reactor without fuel. Insufficient fuel equals no electricity production, and all bets are off.

Names worth knowing:

Cameco ($CCJ) — Vertically integrated through Westinghouse. Mine + mill + converter + 49% of dominant Western reactor and fuel business. The single cleanest stack play.

Centrus Energy ($LEU) — The alternative bottleneck. Highly speculative, policy-dependent, but unrivaled in its domestic position.

7 & 8. Enrichment & Conversion

To make a reactor work, you have to take ordinary uranium-238 and concentrate the rare form of it that splits when struck by a neutron. That dangerous form is called uranium-235. Natural uranium is less than one percent uranium-235. Conventional reactor fuel needs three to five percent. Alternative reactors like SMRs need ten to twenty. Above twenty percent enters weapons-grade and thus makes regulatory agencies really nervous.

The process is called enrichment, and it requires machines called centrifuges. Centrifuges are tall cylindrical devices that spin at the speed of sound, separating uranium atoms by their tiny differences in weight. They are arranged in long cascades — thousands of machines wired together in series — inside heavily fortified facilities monitored by national security agencies, because the same technology can be used to make weapons-grade material.

Globally, four organizations matter. A European consortium called Urenco. The French national nuclear company Orano. The American company Centrus. And the Russian state nuclear monopoly Tenex, which, until very recently, supplied roughly a quarter of all the enriched uranium used in American reactors.

But in May of 2024, the United States banned Russian enriched uranium imports. The phase-out began immediately and finishes by 2027. A quarter of the country’s nuclear fuel supply has, by act of Congress, been removed from the market. The same legislation provided $2.7 billion in funding to rebuild domestic capacity.

This is the layer where policy and capital are running ahead of the industrial response. There is government money. There are contracts. There is unanimous bipartisan agreement that domestic enrichment must be rebuilt. What there is not, yet, is the actual physical capacity to do the work. The country has effectively decided to construct an entire heavy industry from a depleted starting position, on a timeline of five to ten years, while simultaneously needing the output of that industry to scale at unprecedented rates to feed a fleet of reactors that does not yet exist.

This bottleneck will not resolve quickly. It is structurally durable. And it sits at the very center of the supply chain.

There is one more step in the fuel cycle that almost nobody knows exists.

Before uranium can be loaded into a centrifuge, it has to be turned from a solid into a gas. The uranium that comes out of a mine is a powder. The uranium that goes into a centrifuge has to be a gas — specifically, a chemical compound called uranium hexafluoride.

There are, in the entire Western world, two facilities capable of performing the conversion at commercial scale. One is in Ontario, Canada, operated by Cameco. The other is in southern Illinois, operated by Honeywell. The Illinois facility was actually closed for six years, between 2017 and 2023, because there was not enough demand to keep it running. It is the only one in the United States.

The price of conversion services tells the story. In 2017, a kilogram of converted uranium cost about six dollars. By 2024, the same kilogram cost forty. Almost a 7x increase in 7 years, for a service that almost nobody outside the industry has ever heard of. And it’s not because it’s harder, it’s because there’s more demand.

Prices move first. Capacity follows, eventually. In that gap are huge amounts of profit.

Names worth knowing:

Centrus Energy ($LEU) — The only US-owned, US-operated enricher and the sole domestic high-purity uranium producer.

Cameco ($CCJ) — Major converter plus mining and fuel. The conversion exposure is buried inside the larger story. They operate from the ground up all the way to level 6.

Honeywell ($HON) — While the converting business is tiny for them, it’s still a huge player in the nuclear trade.

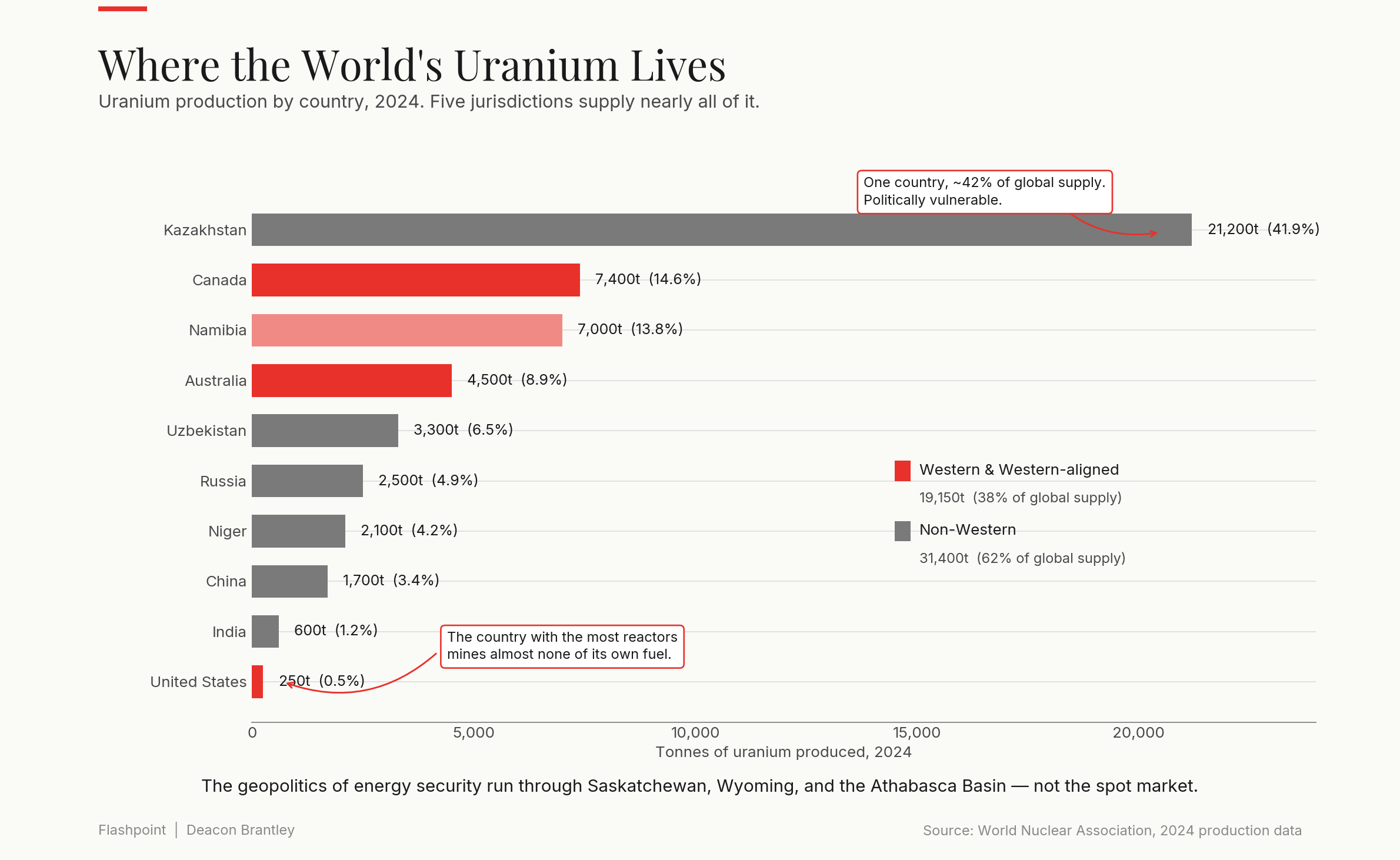

9. The Mine

This is where the rock first leaves the ground.

There are essentially two ways to mine uranium. The first is the way you imagine — a hole in the ground, miners in hard hats, trucks of ore hauled to a mill. This is how the highest-grade uranium in the world, in the Athabasca Basin of northern Saskatchewan, is extracted. The quality there is extraordinary. A ton of Athabascan ore can contain more than a hundred pounds of uranium. Compare that to copper mining, where a ton of ore might contain ten pounds if you’re lucky.

The second method is called in-situ mining. In Wyoming, Texas, and across most of Kazakhstan, uranium is dissolved in groundwater within sandstone formations far underground. In-situ mining doesn’t move any rock at all. A chemical solution is pumped underground, dissolves the uranium where it sits, and is pumped back to the surface for processing. While the quality of the ore is much lower, the capital costs are much less.

The companies that matter at this layer are concentrated. The Canadian firm Cameco operates the highest-grade mines in the world in northern Saskatchewan. The Kazakh state producer Kazatomprom is the largest single uranium company on earth, operating wellfields across central Asia. An American company called Energy Fuels owns the only operating conventional uranium mill in the United States, in Utah, and has a side hustle processing rare earths through the same facility. The most important undeveloped uranium deposits in the Western world sit inside development-stage Canadian and American companies that have not yet broken ground.

The geopolitics of this layer matter more now than they have in fifty years.

Before 2022, where uranium came from was barely a question anyone asked. After Russia’s invasion of Ukraine, it became one of the central questions. Russian uranium has been pulled out of the Western market. Kazakh uranium still flows, but every Kazakh ton is now politically vulnerable in a way that Canadian and American tons are not. The premium on Western-sourced uranium that did not exist five years ago has become structural.

Where the next ton comes from will define the next decade of energy policy.

Names worth knowing:

Cameco ($CCJ) — McArthur River and Cigar Lake. Tier-1 jurisdiction (Canada). The benchmark.

Kazatomprom ($KAP) — Largest producer globally. ISR across Kazakhstan. Lower cost, higher geopolitical risk.

Energy Fuels ($UUUU) — White Mesa Mill in Utah — the only US conventional mill. Convergent uranium + rare earths trade.

10. The Earth

At the very bottom of everything is geology.

Uranium isn’t evenly distributed across the earth’s crust. The high-grade deposits are concentrated in a small number of geological formations, in a small number of countries.

The Athabasca Basin in Canada — a remote, frozen region the size of New Mexico — contains the richest uranium deposits ever found. Wyoming and Texas sit on top of low-grade sandstone formations perfectly suited to ISR mining. Kazakhstan has more of the same. Australia holds significant reserves but has spent decades arguing internally over whether to develop them. A handful of African countries, including Namibia and Niger, contribute to the rest of global supply.

Outside of these places, uranium deposits are few and far between.

The dynamic that defines this layer is time. A uranium deposit discovered today can’t produce a single pound of fuel for ten to fifteen years. The permitting, the engineering, the environmental review, the financing, the construction — none of it can be meaningfully accelerated.

Every pound of uranium the world is going to consume in the next decade has to come either from a mine that already exists, from a project already deep in development, or by running the existing mines harder. That’s why Energy Fuels’ restart and expansion of its White Mesa mill complex in Utah is such a big deal — and why every announcement out of the Athabasca development names matters more than the spot price.

All the uranium the world’s nuclear energy sector uses comes from a very small part of the world.

11. The Trade

And we’ve made it, all the way to the bottom of the stack.

This isn’t a commodity trade. It isn’t an AI trade either; the hyperscalers don’t care which atom splits, only that it does so reliably for the next twenty years. And it isn’t a utility trade in any conventional sense. These are not rate-of-return businesses anymore — they’re vehicles for the four largest balance sheets in human history paying premium prices on twenty-year obligations.

What this actually is, is a structural repricing of a complete industrial supply chain that the West allowed to atrophy for thirty years, occurring simultaneously at every layer.

Three forces have converged in a way that has no recent analog.

Insatiable demand. The federal government’s own 2022 forecasts are off by entire New York Cities of power. AI training models get built on five-year horizons against grid infrastructure that takes fifteen. The capacity gap is real, quantifiable, and worsening every quarter.

Supply that can’t respond. Every link in the chain — mines, conversion, enrichment, forging, reactor manufacturing, transmission — takes the better part of a decade to add at meaningful scale. Capacity retired in the 2010s does not come back online in 2027. This is not a cyclical bottleneck. It is structural.

Capital willing to go to any length. Microsoft, Amazon, Google, and Meta have effectively underwritten the next two decades of nuclear electricity prices. These are not speculative offtake commitments. They are contractual obligations from credit-worthy buyers at premium prices that did not exist three years ago.

Any one of those forces in isolation would be interesting. Their intersection is the trade.

There is also a layer underneath the financial one worth naming directly. This is, for the United States and its allies, the most consequential strategic infrastructure rebuild in a generation. The country has decided — quietly, bipartisanly — that it will not enter the second half of the twenty-first century dependent on Russia, China, and Kazakhstan for the fuel that runs its electricity grid. That decision has dollars behind it. The Department of Energy is now, in effect, a project-finance bank. The Loan Programs Office has more capital to deploy than most sovereign wealth funds.

The right way to think about all of this is not as a basket of tickers but as a thesis with multiple expressions. The thesis is: every layer of a structurally constrained supply chain is being asked to scale simultaneously, with the buyer’s contracts already locked, on timelines the supply side cannot meet, with national-security capital flowing in behind it.

The companies covered in this report — the operators, the manufacturers, the enrichers, the miners — are the public-equity expressions of that thesis. Some are operating, cash-flowing businesses with credit-worthy customers locked in for twenty years. Some are pre-revenue narrative bets on engineering milestones that haven’t happened yet. The portfolio question is how much of each to own. The macro question — whether the thesis itself is correct — is what determines whether any of it works.

If the thesis is wrong, it’s wrong because one of three things broke: the hyperscalers walked from their contracts, the policy environment reversed, or the AI buildout stalled. None of those are zero-probability outcomes. None are base cases either.

If the thesis is right, this is the energy trade of the next decade. Not because uranium goes to $200, and not because any single SMR developer ten-bags. Because the entire chain, from the rock to the electricity, is being rebuilt at once, paid for by the four largest companies on Earth, in service of the most important technology being built right now.

It will also determine something larger than any portfolio.

It will determine whether the United States and its allies retain control of the strategic infrastructure that powers the twenty-first century, or whether the energy dependency on Russia, China, and Kazakhstan that the West spent thirty years drifting into becomes permanent.

Flashpoint | Deacon Brantley 26 June 2026

Not financial advice. Always do your own research and take care when trading.

Some selected sources are printed below

Government Legislation, Policy, & Regulatory Reports

U.S. Congress (2024). Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act of 2024 (S.870). Passed 88-2 in the Senate to streamline licensing and incentivize next-generation reactor deployment.

U.S. Congress (2022). Public Law 117-169: Inflation Reduction Act of 2022. Specifically highlighting the creation of federal production tax credits (PTCs) to sustain existing commercial nuclear reactors.

U.S. Department of Energy (DOE) (2022). Annual Energy Outlook 2022 with Projections to 2050. The official power grid demand forecast used as a baseline prior to the AI expansion.

U.S. Congress (May 2024). Prohibiting Russian Uranium Imports Act (H.R. 1042), signed into law May 13, 2024.

U.S. Department of Energy (DOE) Loan Programs Office (2024). Clean Energy Financing Program: Federal Loan Allocations for Nuclear Fleet Restoration and Palisades Plant Restart.

U.S. Nuclear Regulatory Commission (NRC) (2023). Final Safety Evaluation Report: NuScale Power Small Modular Reactor (SMR) Standard Design Certification.

Georgia Public Service Commission (2024). Vogtle Electric Generating Plant Units 3 and 4: Final Construction Audits, Over-Budget Accounting, and Commercial Operation Status.

Hyperscaler Power Purchase Agreements (PPAs) & AI Grid Demand

Constellation Energy & Microsoft Corp. (September 2024). Joint Corporate Announcement: 20-Year Power Purchase Agreement to Launch the Crane Clean Energy Center (Three Mile Island Unit 1 Restart).

Talen Energy / Amazon Web Services (AWS) (March 2024). Commercial Property Transaction Ledger: AWS Acquisition of the Cumulus Data Center Campus Adjacent to the Susquehanna Nuclear Generating Station ($650M).

Google Cloud & Kairos Power LLC (October 2024). Master Power Purchase Agreement and Deployment Framework for Commercializing Next-Generation Fluoride Salt-Cooled SMRs.

Amazon.com Inc. & X-Energy Reactor Company LLC (2024). Strategic Investment Venture: Series C Funding and PPA Commitment for Xe-100 Small Modular Reactors.

Meta Platforms, Inc. (Late 2024). Global Infrastructure Procurement Division: Public Request for Proposals (RFP) for up to 4,000 MW of Continuous Baseload Clean Energy Capacity.

International Energy Agency (IEA) (2024). Electricity 2024: Analysis and Forecast to 2026. Data center power consumption growth metrics driven by frontier large language models (LLMs).

Nuclear Operators, Plant Restarts, & Utilities

Constellation Energy Corporation ($CEG) (2024). Form 10-K Annual Report. Operating fleet economics, license extensions, and non-utility PPA margins.

Constellation Energy & Walmart (June 2026). 15-Year Nuclear PPA Announcement — Dresden Clean Energy Center.

GE Vernova Inc. ($GEV) (2025-2026). Quarterly Financial Disclosures, Nuclear Steam Turbine Backlog Metrics, and BWRX-300 Deployment Updates.

Holtec International (2024). Engineering Feasibility and Safety Systems Review: Restoring the Dormant Palisades Nuclear Plant (Michigan) to Operational Status.

Entergy Corporation & Exelon Generation (2014–2021). Historical Corporate Filings — Economic Closures and Decommissioning of Vermont Yankee (2014) and Indian Point (2021).

Grid Infrastructure & Supply Chain Bottlenecks

Forgent Power Solutions ($FPS) (2025-2026). Annual Shareholder Presentation: High-Voltage Transformer Backlogs and Transmission Grid Expansion Constraints.

U.S. Department of Energy (DOE) Grid Deployment Office (2023). National Transmission Needs Study. Structural capacity deficits and permitting lead times.

World Nuclear Association (WNA) (2024). Global Nuclear Supply Chain Report: Heavy Forging Capabilities, High-Volume Steel Metallurgy.

American Society of Mechanical Engineers (ASME) (2024). Nuclear Components Standards (Section III): Heavy Industrial Capacity and Lead Times for Zirconium and Inconel Specialty Alloys.

Uranium Mining, Geology, & Refining

Cameco Corporation ($CCJ) & Brookfield Renewable Partners (2023). Joint Acquisition Prospectus: Strategic Integration and Purchase of Westinghouse Electric Company.

Centrus Energy Corp. ($LEU) (2024-2026). Operational Milestone Reports: American Centrifuge Plant HALEU Production Scale-Up in Piketon, Ohio.

Energy Fuels Inc. ($UUUU) (2024-2026). White Mesa Mill Operational Strategy: Co-Processing Domestic Uranium Ores and Heavy Rare Earth Element (REE) Concentrates in Utah.

Saskatchewan Ministry of Energy and Resources (2025). Geological Survey and Ore Grade Audits of the Athabasca Basin Uranium Mining District.

Wyoming State Geological Survey (WSGS) (2024). In-Situ Recovery (ISR) Uranium Mining Projects and Sandstone Roll-Front Deposit Inventories in the Powder River Basin.

Historical Case Studies & Foundation Data

President’s Commission on the Accident at Three Mile Island (1979). The Kemeny Commission Report: The Need for Change: The Legacy of TMI.

International Atomic Energy Agency (IAEA) (1986). The Chernobyl Accident: INSAG-1 Post-Accident Review Meeting Summary Report.

Fukushima Nuclear Accident Independent Investigation Commission (NAIIC) (2012). The Official Report of the Fukushima Nuclear Accident Independent Investigation Commission.

If you made it down here, thanks so much for reading. :)

Great post! I finally understand, albeit only a little bit, about nuclear energy which I've heard so much about through stocks like OKLO.

Many thanks for the extensive research and article. Very interesting and well done!

Which of the companies active in this field would currently be your favourite investment?