Space: The Deep Dive

The space buildout will define the next century. Here's the breakdown.

Fifteen billion miles from Earth, a spacecraft the size of a compact car is falling deeper into the void at 38,000 miles per hour.

It was launched in 1977. It carries a gold record with greetings in fifty-five languages, recordings of waves and animals, and photographs describing daily life on Earth fifty years ago.

Voyager sees nothing but darkness ahead. Behind it, a microscopic pale blue dot growing dimmer by the day.

But if it turned its cameras back toward that dot right now, it would see something very different from what it left behind.

It would see cargo landers heading for the lunar south pole.

It would see prototype space stations under construction in Long Beach, and Chinese constellations climbing to fill the same orbit.

It would see a web of over ten thousand satellites, most of them launched in the last four years, pointed at farmhouse dishes in Iowa, at NORAD antennae in Colorado, at Chinese naval formations in the South China Sea, and at Google data processing facilities.

It would see rocket flames lighting up the West Texas desert every four days.

And below all of it — past the antennas, past the factories, past the fiber running under the desert — it would see something older and slower than any of it. A drill bit chewing through dense rock at three inches per hour in Mountain Pass, California, extracting the ore that will end up as a key magnet inside the propulsion system of the next satellite pointed back at Earth.

The supply chain runs both ways.

Voyager is where the money ends up. Mountain Pass is where the money starts.

Space is no longer a science project. It is the next twenty-year industrial buildout. Twelve layers deep, from a vein of rock in California all the way up to a spacecraft fifteen billion miles from home. Trillions of dollars of infrastructure being built, designed, and launched — all on capital that has finally decided space is worth owning.

This is one of the most important buildouts in humanity’s history.

I’m breaking it all down.

Welcome to Space: The Deep Dive.

0. Space Race Two

Space Race One began on October 4, 1957, when a Soviet radio transmitter the size of a beach ball called Sputnik started beeping over Washington, D.C.

It ended eighteen years later, when American and Soviet astronauts shook hands in orbit and the industry that had built the Saturn V began, quietly, to atrophy.

For the next forty years, space was a government research project, underfunded and far-removed from commerce and industry.

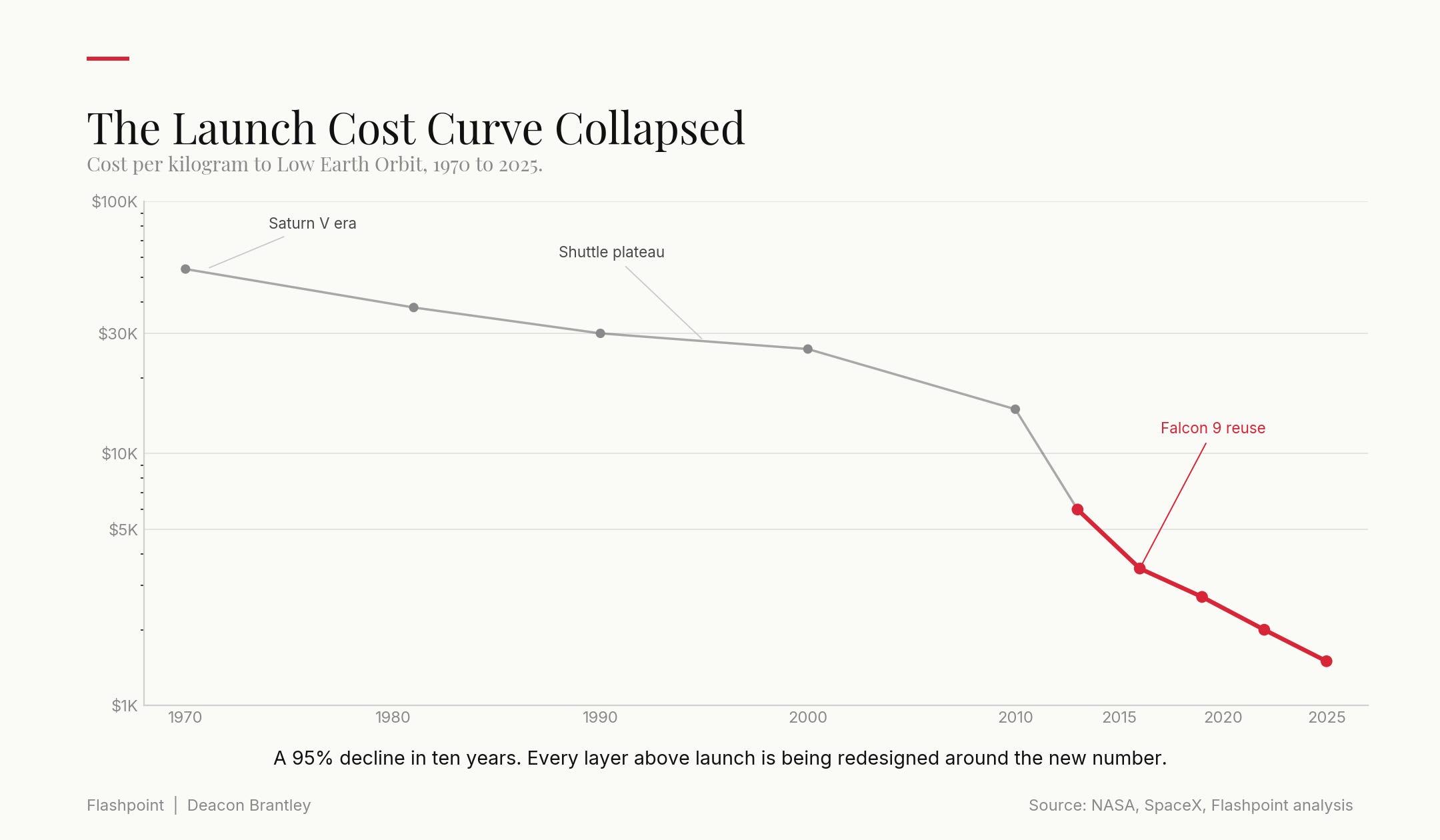

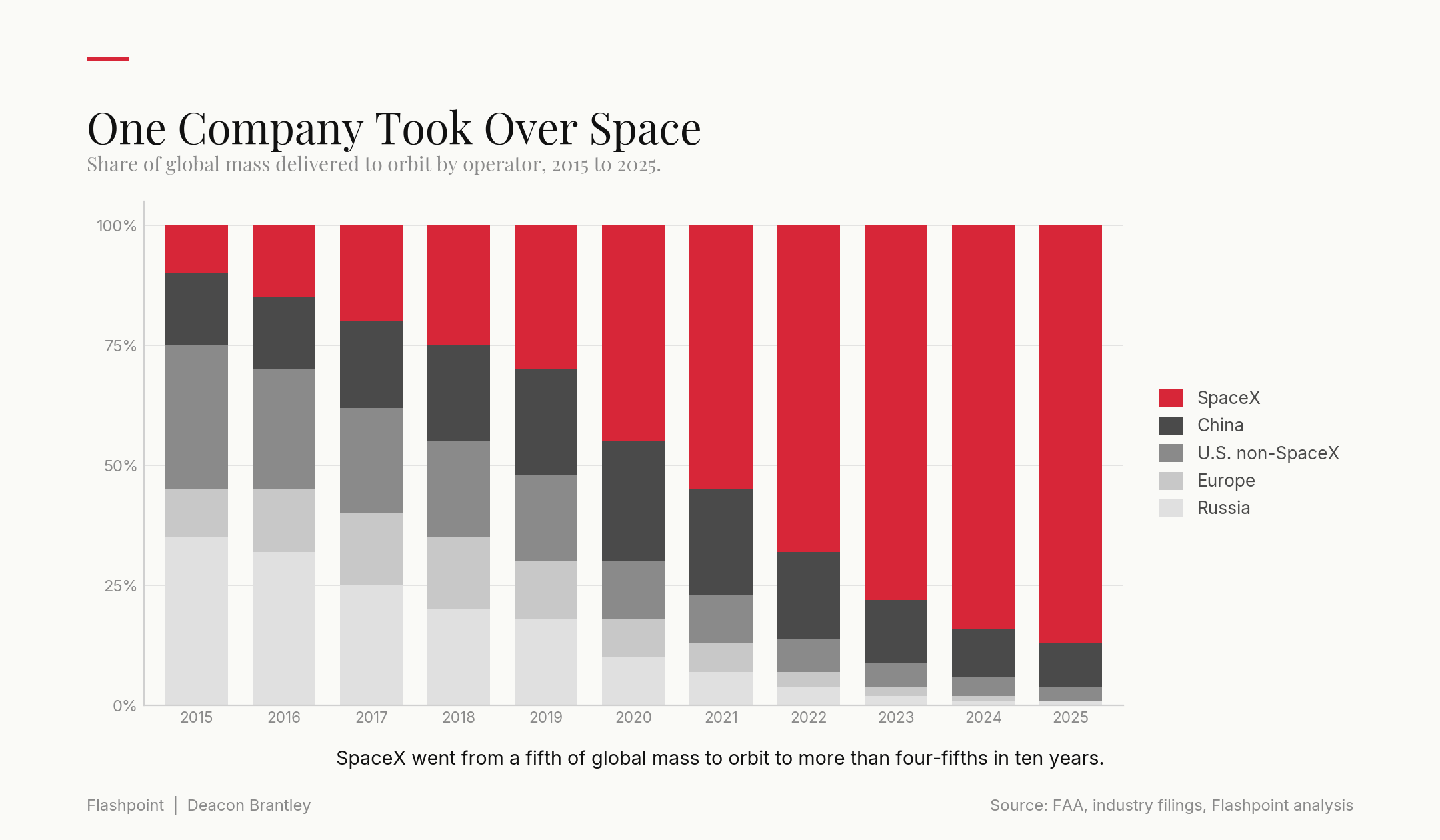

Then, in 2015, a rocket landed at Cape Canaveral, Florida.

That single event kicked off the collapse of the cost curve. Ten years later, the same company launches roughly 85% of the world’s mass to orbit at prices its competitors cannot match. They’ve even launched a Tesla Roadster with a mannequin driver in a spacesuit into space.

In addition, their Starlink constellation exceeds ten thousand active satellites and grows by roughly a hundred every single week. They invented modern reusable rockets at scale. And their stock went public in a recent blockbuster IPO at a valuation north of $1.8 trillion. Obviously, this company is SpaceX.

And they’re the reason Space Race Two has begun.

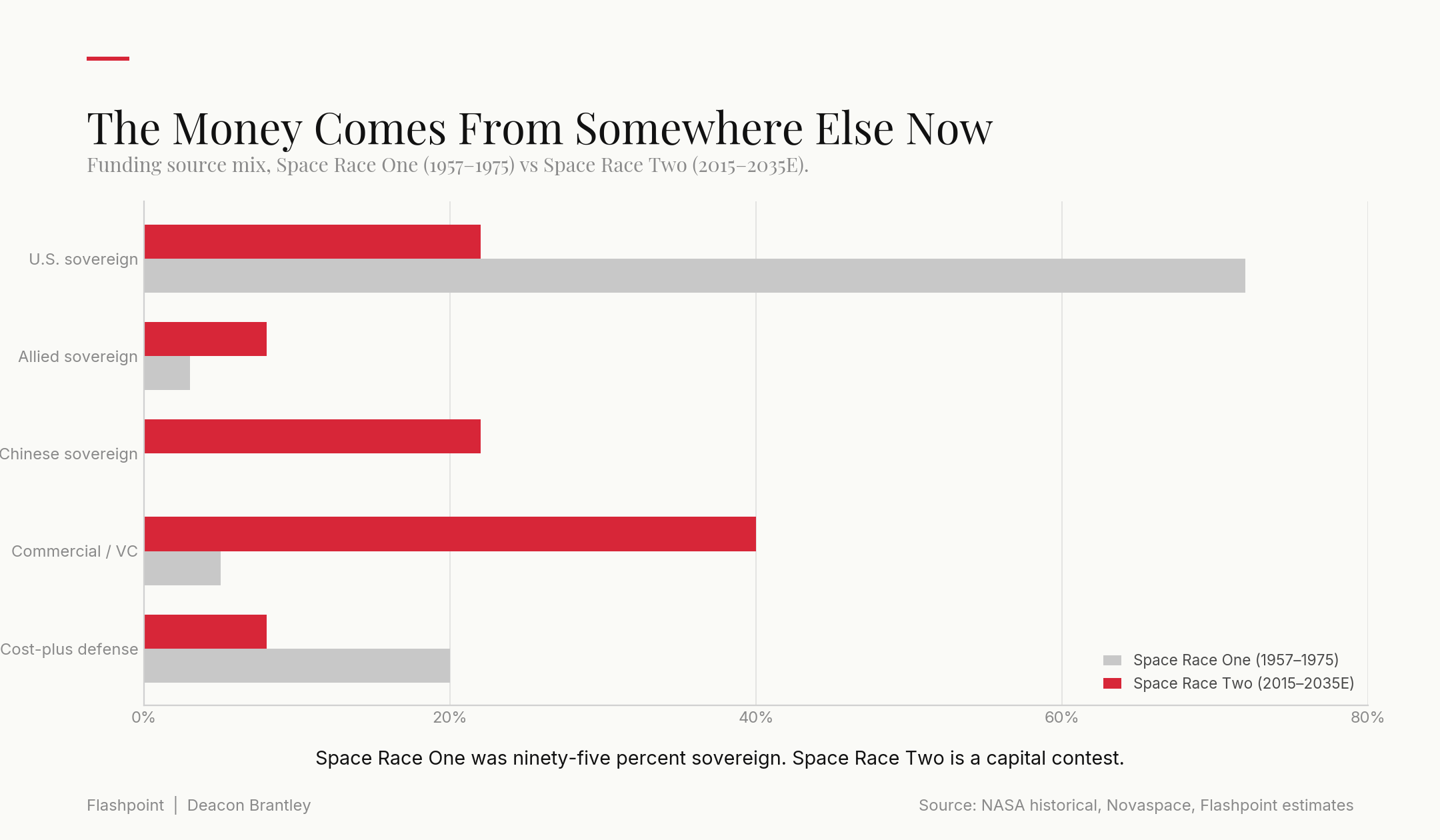

The difference between Space Race One and Space Race Two is that the first was ideological, but the second is industrial.

Space Race One was a prestige contest between two governments. It was a symbolic mission with no real economic gain. Space Race Two is an all-or-nothing corporate buildout split between four forces: the American and Western commercial buildout, the Chinese sovereign buildout, allied organizations trying to hedge both, and the U.S. Department of Defense trying to guarantee its architecture survives into the 2100s.

Every one of those forces is willing to spend hundreds of billions of dollars — even trillions of dollars — all to ensure their architecture is the one or two that reign supreme. McKinsey estimates the value of the space economy will reach $1.8 trillion by 2035 and AFPC is claiming a $10 trillion dollar valuation by 2050.

The main catalyst on the American commercial and governmental sides is the Golden Dome executive order signed in January 2025 — a Pentagon commitment to a space-based missile defense architecture in the hundreds of billions of dollars, with a decade-long execution horizon.

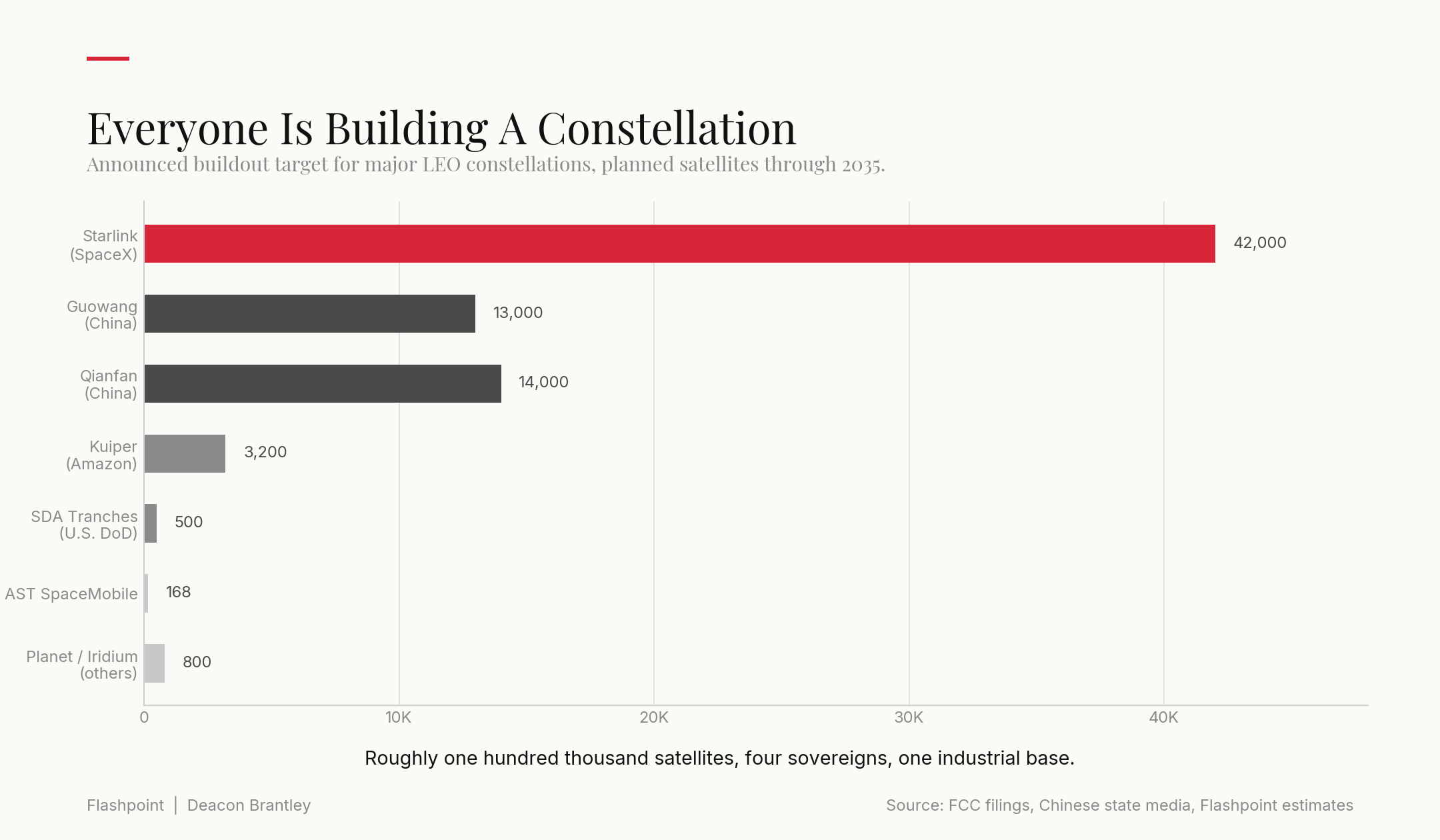

On the Chinese side, the Guowang and Qianfan constellations combine for a stated buildout target north of twenty-six thousand satellites.

On the AI/commercial side, the compute buildout is running into physical constraints — spectrum, ground station capacity, satellite-based data pipes, etc. — that make the space layer indistinguishable from the AI layer inside of five years.

The reason all of this is happening at once is that the cost of getting to orbit fell by roughly 95% in a decade, and now that opens up the space economy for commercial and defense purposes.

Elon Musk’s stated goal is to make humanity multi-planetary. Whether you believe he’ll get there is beside the point. What matters is that his stated goal has already reset the demand curve for launch, which has already reset the demand curve for satellites, which has already reset the demand curve for rad-hard chips, superalloys, and rare earth magnets, which justifies the influx of over a trillion dollars in predicted spending by 2035.

The buildout starts, physically, at the bottom of the stack. From the rock in the ground, working its way up to the farthest thing humanity has ever built.

Let’s start below the surface, rise past a launch facility, and end up billions of miles away.

1. Below The Surface

Altitude: underground

Just like with nuclear energy, the buildout starts underground.

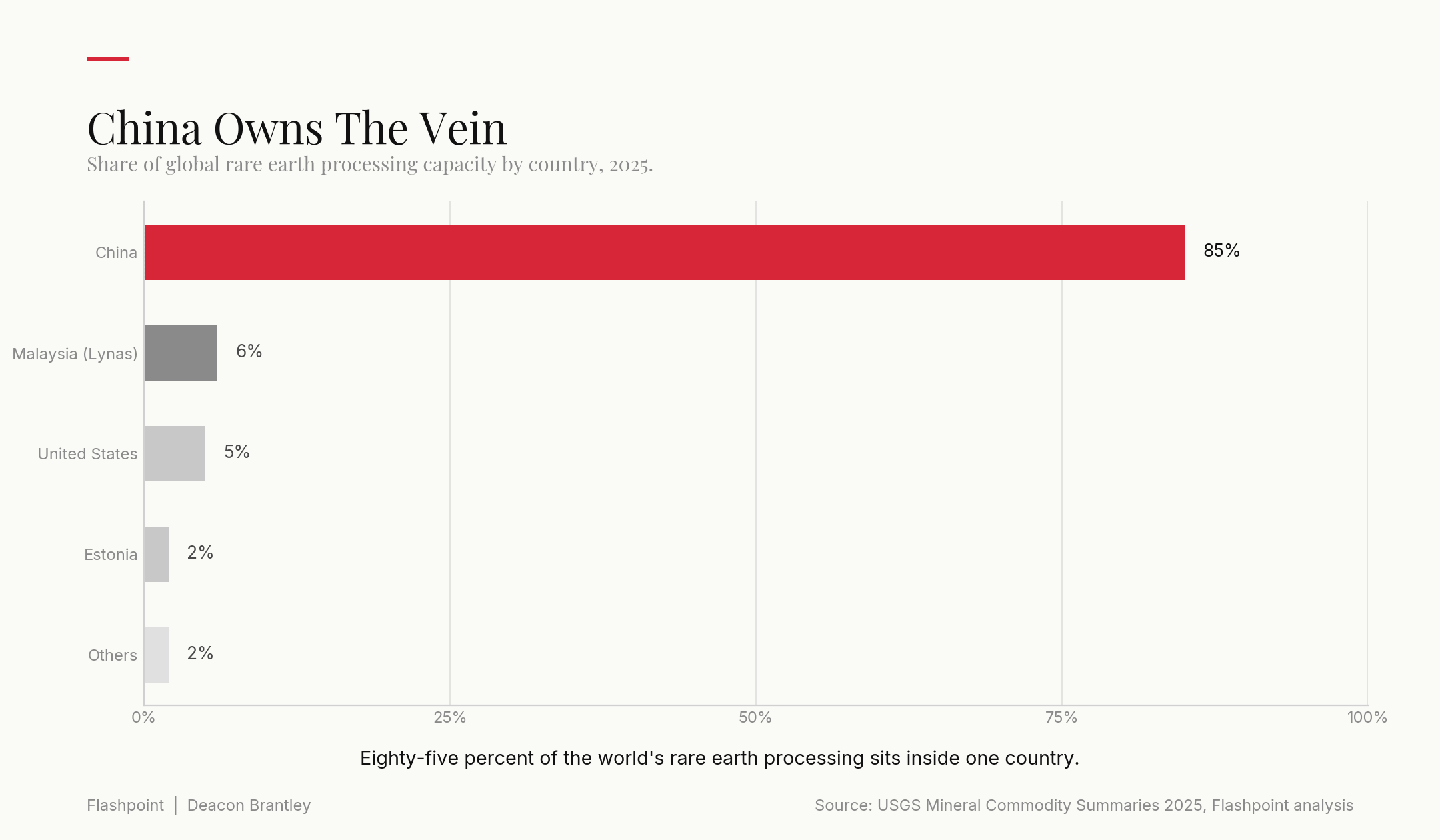

Every permanent magnet needs neodymium, dysprosium, and samarium. Every one of those materials, at current global processing capacity, flows through Chinese companies.

The story extends past magnets. Titanium is the primary structural material of every serious spacecraft. Tantalum is in every capacitor. Gallium and germanium are the substrates for the rad-hardened chips at the next layer up. Lithium is in the batteries. Cobalt is in the superalloys that survive rocket exhaust.

Approximately 85% of the world’s rare earth processing capacity is Chinese. The mining is more distributed — Australia, the United States, and Africa produce meaningful ore — but the separation and processing steps that turn ore into magnets are geographically concentrated in a way that isn’t tolerable in the second space race.

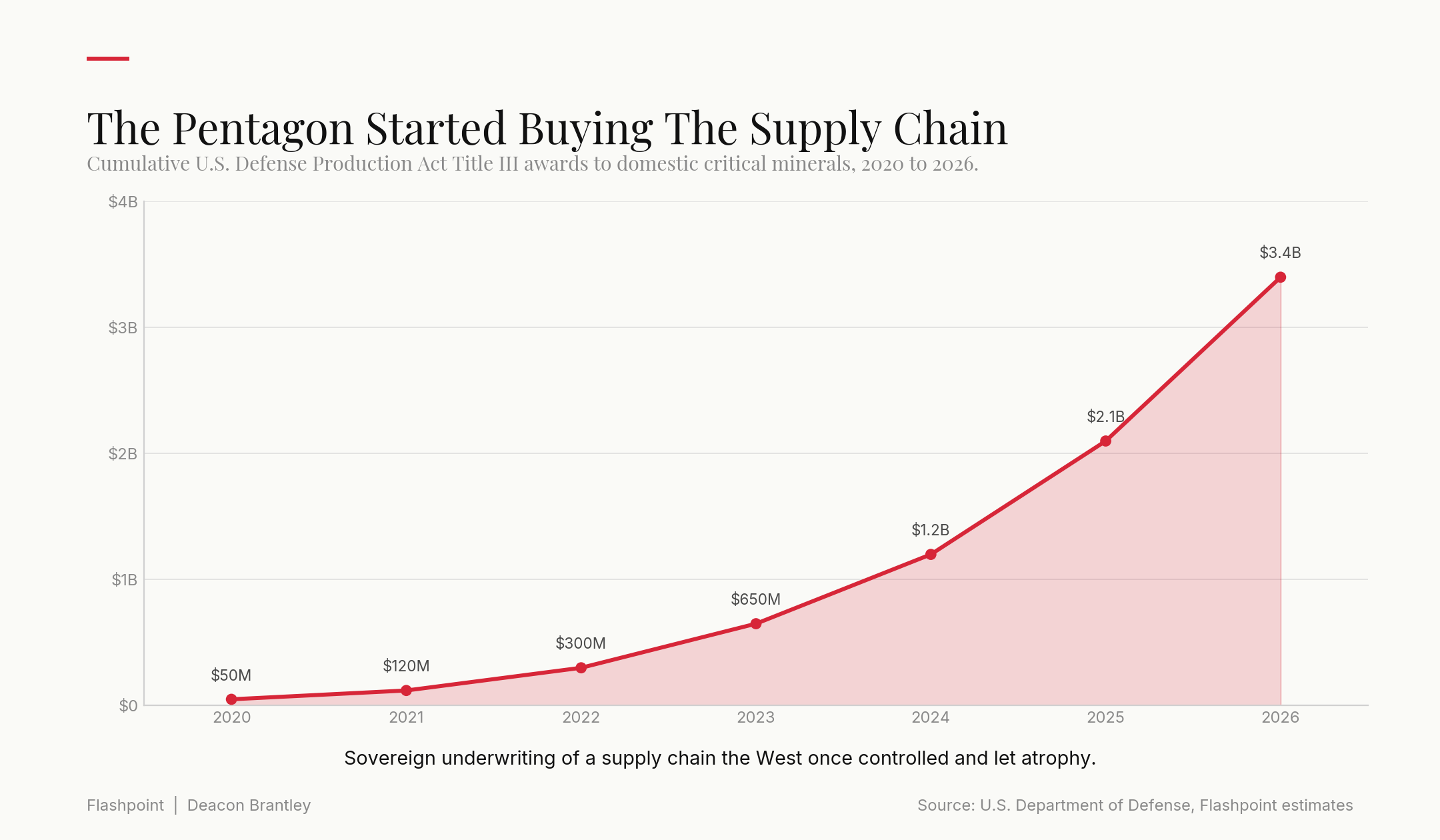

Reversing thirty years of decline will take a decade of investment. And that decade has already started. The Department of Defense has funded MP Materials directly, taken equity stakes in domestic rare earth processors, and committed to purchasing materials from Western companies at price floors well above market levels.

This is exactly the pattern the Department of Energy followed with uranium enrichment three years ago. Facing a hollowed-out supply chain, they stepped in with economic incentives that flipped the script from decline to progress.

Above the raw ore sits the metallurgy tier: titanium mills, superalloy processors, carbon fiber lines, and high-strength steel producers. This is where ore becomes ready-to-machine. Western capacity here is single-sourced in most categories — the same chokepoint pattern that will repeat at every layer above.

For the Pentagon, paying triple the market rate for a domestic supplier is cheap compared to losing the industrial base entirely. That premium is what the operating margin will look like at the miner once the offtake agreements clear. It is the same trade that repriced the nuclear fuel cycle three years ago.

Key names:

MP Materials ($MP): the only fully-integrated rare earth miner in the West. The Pentagon owns a stake, guarantees a price floor, and treats it like a strategic asset. Because it is.

Energy Fuels ($UUUU): a uranium miner with a rare earth side hustle that ties the nuclear thesis and the space thesis to the same balance sheet. Rare double-exposure.

USA Rare Earth ($USAR): the West Texas processor with a Defense Department contract most retail investors haven’t found yet.

Allegheny Technologies ($ATI): if it flies fast, it’s probably built with ATI titanium.

But rock is just rock.

Someone has to turn rocks and ore into the specialized components lifting rockets off the ground.

2. Industry

Altitude: the factory floor

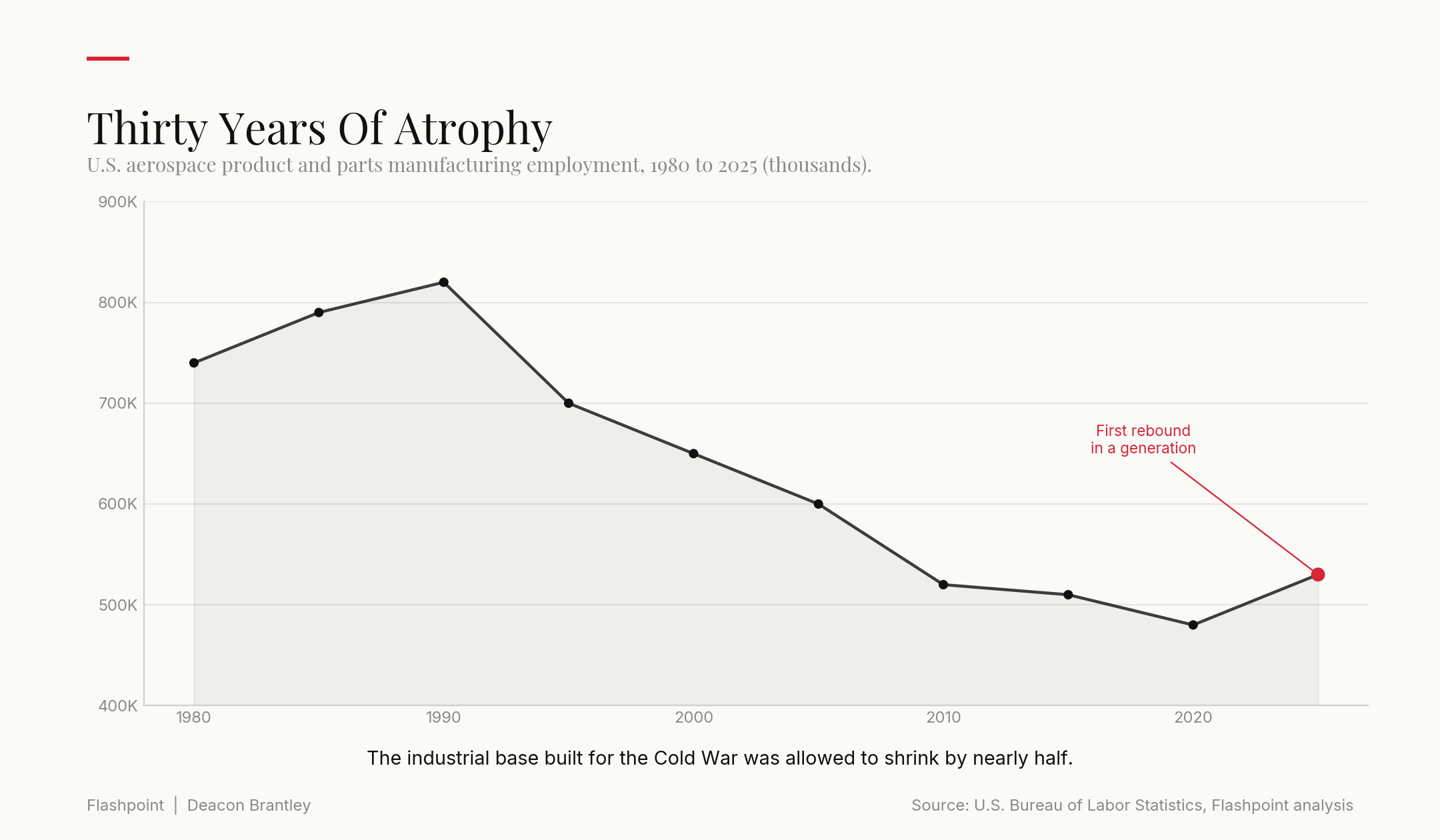

Above the mineral veins is where the industrial base of the space economy lies. And it is what breaks first in the space buildout.

Manufacturing capacity for aerospace-grade hardware has been declining for thirty years. During the shuttle era, the U.S. built roughly a dozen launch vehicles per year and a modest number of satellites. During the Starlink era, it needs to build a thousand satellites per month.

The canyon between demand and supply cannot be fixed by just capital alone. America needs to train new workers, establish labor pipelines, re-open factories, and allocate more attention to the aerospace sector.

The prime contractors — the companies assembling the major systems — are one story. Boeing, Lockheed, and Northrop are all scaling. But they are gated by the tier below them: the specialty subcomponents tier. Ion thrusters. Cryogenic tanks. Solar cells. Propulsion systems. Heat shields. Et cetera.

Every one of these components has a small number of suppliers. Many are single-sourced. Most had their production capacity cut in the 1990s and 2000s and are only now beginning to rebuild it. When a satellite operator needs ten thousand specialized permanent magnets a year and the supplier base can only produce two thousand, prices skyrocket.

The same kind of atrophy that’s plaguing the nuclear energy buildout exists in the space industry — a small number of qualified suppliers, most of them single-sourced, with pricing power they haven’t had in decades. The Pentagon and NASA are aware of it. The IRA-adjacent industrial policy tools — Defense Production Act allocations, DoD Manufacturing Innovation Institutes, allied co-production agreements — are all being pointed at this layer. This is where the sector bottlenecks are in the next couple years. Prices are already sharply moving upward. Satellite operators are already signing multi-year agreements to lock in supply. The single-source suppliers here are re-rating on visible order books, and the ones still private are the most valuable IPO pipeline in the sector.

This tier is the space economy's version of the memory and chip subcomponents inside the AI buildout — the SanDisks, the Microns. The names most investors ignore until they realize every dollar of end-market growth flows through them. And the pricing dynamic here is even more brutal than it is in AI, because launch operators and satellite manufacturers can't afford to wait for a better price. Any delay costs them a launch window, a constellation slot, or a Pentagon contract. Speed and quality come first. Price comes a distant third. The suppliers know it, and they're charging accordingly.

Key names:

Redwire ($RDW): a space infrastructure pure-play — components, deployable arrays, lunar hardware. If it flies to space and it isn’t a rocket, Redwire probably had a hand in it.

Karman Space & Defense ($KRMN): propulsion, fairings, thermal protection for almost every Western launch vehicle and hypersonic program. Top position in my personal portfolio for a reason.

HEICO ($HEI): the roll-up nobody talks about. Twenty years of quietly acquiring aerospace parts makers, now sitting on a portfolio no one else can replicate — and pricing power to match.

3. Software

Altitude: in the cloud

This is the layer that turns pixels, radio waves, and telemetry into intelligence. A raw satellite image is a file. An analyzed image, taken from a satellite peering directly over a Chinese military base, is a piece of intelligence someone will pay millions of dollars a year for.

Golden Dome will be a software program as much as a hardware program. The Space Development Agency’s proliferated warfighter architecture is a network. Missile warning fusion, orbital debris tracking, threat identification — all software problems. Agriculture, insurance, and commodity trading buy satellite data too, but the dollar volume and the pricing power live on the defense side.

This is the demand-side hyperscaler analog for the space economy. In the nuclear thesis, four hyperscalers with two hundred billion dollars of annual profit set the floor price for electricity. Here, one buyer with a trillion-dollar horizon sets the floor price for space-derived intelligence. If Golden Dome’s contract book accelerates, the entire cascade beneath it compounds. If it slows, everything slows with it.

Key names:

Palantir ($PLTR): the Pentagon and half the Fortune 500 pay Palantir to make sense of everything they collect. If there’s a data-to-decision pipeline in defense, it probably runs through them.

BlackSky ($BKSY): runs its own EO constellation and sells the data directly to sovereign customers. Small-cap, government-anchored, and the kind of asymmetric setup I keep coming back to.

4. Data Capturing

Altitude: ground level

Every signal from every satellite above has to land somewhere.

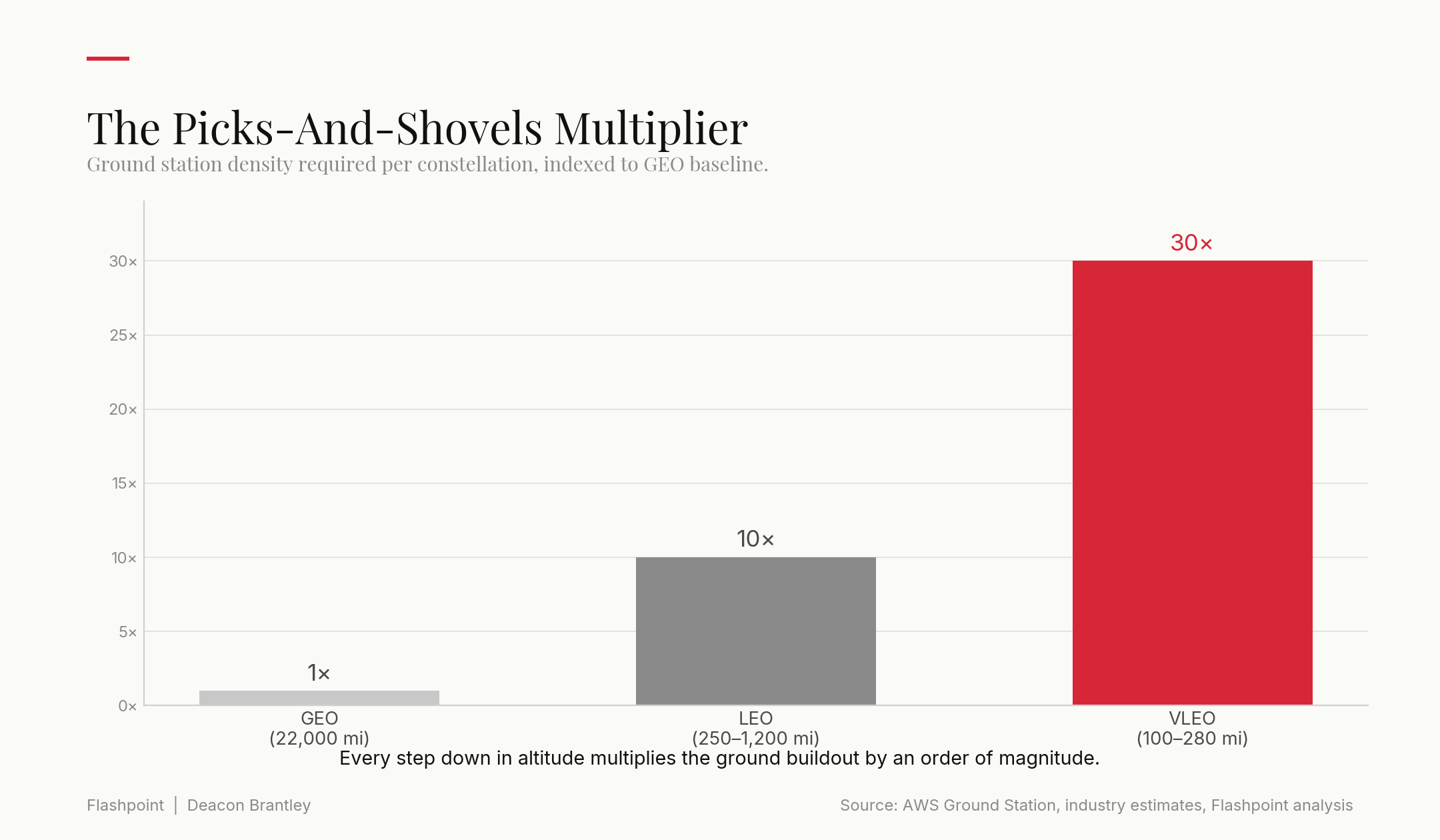

The ground segment is the terrestrial infrastructure that makes space useful. Antennas, teleports, phased arrays, gateway stations, mission control centers, and the fiber networks that connect them all to the internet and to the customers who pay for the data.

Traditional GEO (geostationary orbit) satellites needed a modest number of ground stations, because their satellites hung in place. LEO (low Earth orbit) constellations need ten times as many. VLEO (very low Earth orbit) constellations may need thirty times as many.

Every Starlink dish on a farmhouse roof is a data point. The commercial ground network is being rebuilt at hyperscaler speed.

The most consequential development in the ground segment is the entry of the cloud providers. Amazon Web Services launched AWS Ground Station in 2018. Microsoft launched Azure Orbital in 2020.

Both offer a major service: a satellite operator can pay by the minute for antenna time, rather than build a global network of their own. This is the same commoditization pattern that hit computing infrastructure a decade earlier. It compresses the moat for legacy ground station operators. It expands the addressable market for the picks-and-shovels vendors.

The ground segment is where the constellation buildout stops being invisible and starts being physical: every rooftop dish and every hyperscaler antenna field is a point of LEO or VLEO data transference.

Key names:

Viasat ($VSAT): the broadest ground terminal footprint on Earth. Legacy business, but every LEO operator eventually leans on their infrastructure.

Kratos Defense ($KTOS): ground command-and-control for both commercial constellations and Pentagon programs. Increasingly essential as LEO gets crowded.

Amazon ($AMZN): known for e-commerce and cloud, but AWS Ground Station rewrote the segment’s economics overnight. Every incumbent has been playing catch-up since 2018.

But antennas only catch signals.

The satellites emitting those signals had to be lifted there first — and that is where the entire stack goes through a single tollbooth.

5. Launch

Altitude: the launch pad

Launch is the strategic bottleneck of the entire space economy. It is the space-economy equivalent of what conversion and enrichment are to the nuclear stack — an obscure, capital-intensive processing tier that most investors never think about, but that every layer above depends on.

The numbers are stark.

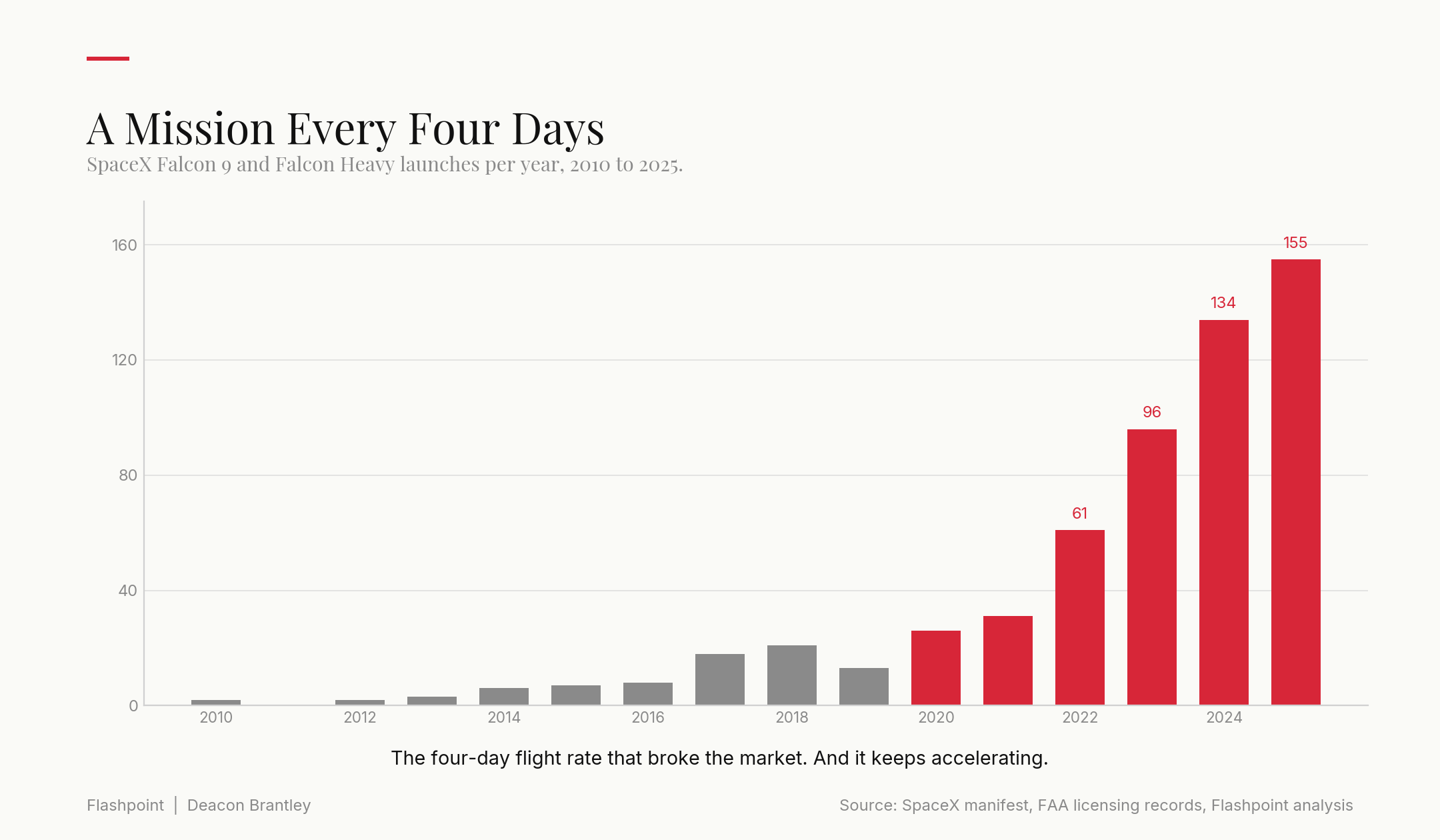

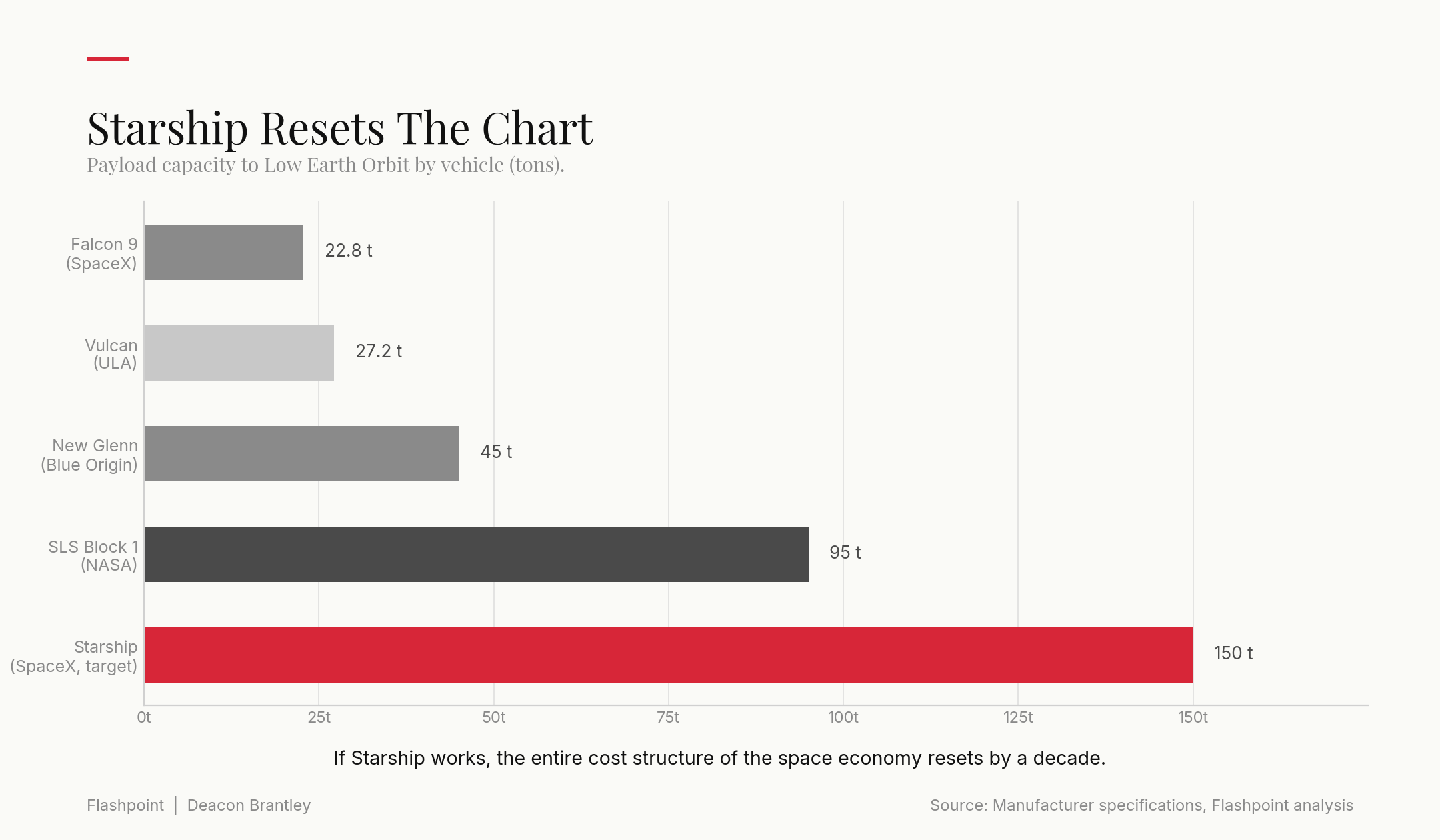

In 2024 and 2025, SpaceX launched more mass to orbit than every other company and every other country in the world combined. Its Falcon 9 flies a mission approximately every four days. Its Starship program, if it succeeds, will reduce cost-per-kilogram by another full order of magnitude.

No one else is close. Rocket Lab is the credible number two on the small side, with Electron in service and Neutron approaching first flight. United Launch Alliance flies Vulcan on national security contracts. Blue Origin flies New Glenn. Firefly, Relativity, and a handful of startups fight for the remaining share.

The consequence of this concentration is that the pricing floor for the entire space economy is set by a single company. If SpaceX raises Falcon 9 prices by 20% next year, every constellation operator and every government pays it. There isn’t an alternative.

That is what a strategic bottleneck looks like. Prices move first. Capacity follows years later. Whoever wins number-two on the medium-lift curve — Neutron, New Glenn, or a Chinese entrant — gets a decade of pricing power while the world waits for supply to catch up. That question is the most important open bet in the sector.

Key names:

SpaceX ($SPCX): the single most important company in the space buildout. Roughly 85% of global mass to orbit, sets the pricing floor for everything above, and now the largest IPO in history. If Starship works, the whole cost curve resets down another decade.

Rocket Lab ($RKLB): the only credible SpaceX competitor. Electron is proven on small-lift; Neutron takes aim at the Falcon 9 franchise. Generational upside if the second rocket lands.

Karman Space & Defense ($KRMN): the propulsion supplier feeding every Western launcher in the race for number-two. A pick-and-shovel that wins regardless of who wins the race.

But launch is only the beginning.

Sixty-two miles later, it crosses into the region where the atmosphere gives up and defense budgets take over.

6. The Karman Line

Altitude: 62 miles up, the line between the atmosphere and space

Sixty-two miles above the Earth is the internationally recognized boundary between the atmosphere and space.

Everything at or just below that altitude is the territory of defense.

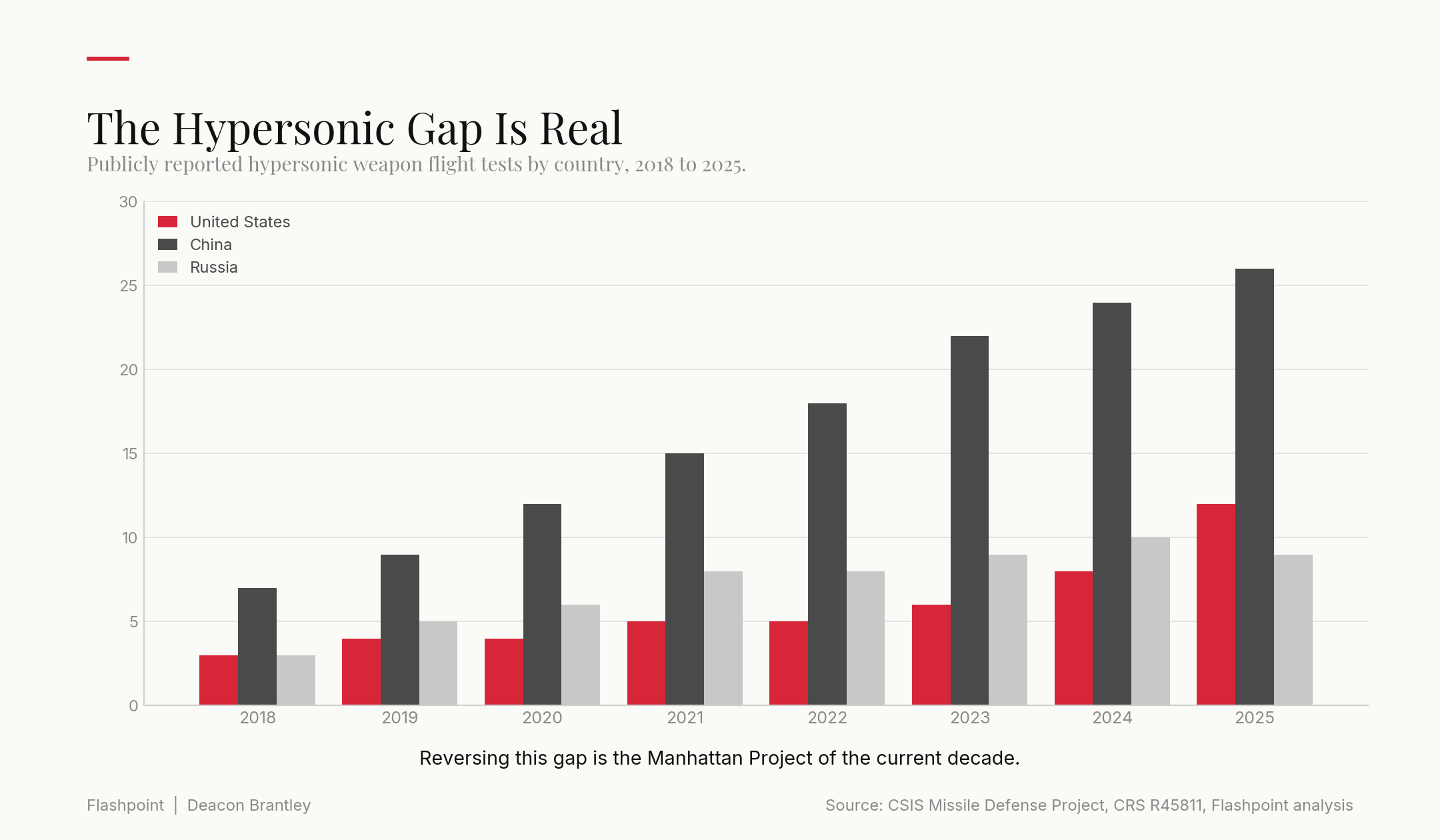

Hypersonics — vehicles that maneuver at Mach 5 or faster inside the upper atmosphere — are now the fastest-growing classified project category at the Pentagon. It is also the most consequential. Both China and Russia have deployed hypersonic weapons the United States cannot yet reliably intercept. Just look at this chart:

Reversing that gap is the Manhattan Project of the current decade, and it is where the Pentagon’s most secret money is being spent. The contracts flow through the same defense companies that dominate the layers above and below: Lockheed, Northrop, Raytheon.

But the propulsion, the materials, and the guidance systems flow through a smaller set of specialized suppliers, many of them the same names flagged as bottleneck suppliers at the industry layer.

That is the key facet of the trade: hypersonics doubles the demand pressure on an industrial base that constellation operators are already trying to buy out, and when two of the decade’s most important defense priorities compete for the same qualified suppliers, prices don’t stay still.

They skyrocket.

Suborbital tourism (Virgin Galactic, Blue Origin’s New Shepard) is a footnote to this layer. Hypersonics is what matters.

Key names:

Lockheed Martin ($LMT): the hypersonics prime on almost every major classified program — ARRW, Long-Range Hypersonic Weapons, and a lot more the public doesn’t get to see.

RTX ($RTX): the missile and interceptor giant scaling into hypersonic defense. If the U.S. builds a working kinetic kill vehicle for hypersonics, it’s probably an RTX contract.

BWX Technologies ($BWXT): specialty materials for the parts that have to survive Mach 5 without melting. Small ecosystem, single-source in several categories.

Karman Space & Defense ($KRMN): shows up again. Propulsion and airframes for both launch and hypersonics. Two of the most important defense buildouts of the decade running through one supplier.

Rise another hundred miles.

You enter the newest region of usable orbit — where two markets are being born at the same time.

7. VLEO & Sub-LEO

Altitude: 62 to 280 miles away

Between the Karman line and the standard LEO constellations, two markets are emerging simultaneously.

The first is the post-ISS commercial station economy. The International Space Station is scheduled to deorbit in 2030 or 2031. NASA’s Commercial LEO Destinations program has committed approximately $8 billion to seed the private replacements: Axiom Space, Vast Space, Voyager Technologies (Starlab), Sierra Space (LIFE habitat), and Blue Origin (Orbital Reef). Each is anchored by a prime contractor and a sovereign off-take agreement. Each is targeting operational status in the early 2030s.

This is the same structural setup as commercial launch in 2015 — sub-scale today, structural by 2035, underwritten by NASA and DoD demand. Every one of the primes involved sees this as their generational infrastructure play.

The second sub-LEO market is Very Low Earth Orbit. VLEO is the region between roughly a hundred and three hundred miles up — low enough that atmospheric drag becomes a serious problem, and low enough that sensor resolution, communications latency, and refresh rate improve step-function. The enabling technology is air-breathing electric propulsion: satellites that ingest residual atmospheric molecules and use them as reaction mass to fight drag.

VLEO’s primary customers today are mostly classified: tactical DoD reconnaissance programs, with a growing commercial edge in sub-meter Earth observation and low-latency point-to-point comms. The pricing power will accrue to whoever solves the propulsion problem at scale, and the propulsion suppliers are the same ones flagged as bottleneck names at Layer 2. Together, sub-LEO establishes the shape of the 2030s orbital economy before the 2020s buildout is even finished — stations at 250 miles, VLEO tactical fleets at 150 miles, both underwritten by two sovereigns, both funneling work down through the same industrial base.

Key names:

Voyager Technologies ($VOYG): the public-market way to own a piece of the commercial space station buildout. Starlab is NASA-backed, and NASA doesn’t back things it doesn’t intend to fly.

Redwire ($RDW): shows up in almost every commercial station bid — components, habitats, deployables. If any of them fly, Redwire benefits.

Boeing ($BA): the prime on Orbital Reef with Blue Origin, and the only Western operator with decades of live station operations experience from the ISS.

AST SpaceMobile ($ASTS): satellite-to-cellphone at LEO and lower. If the phone in your pocket talks directly to a satellite by 2030, it’s probably going through ASTS.

Rise another two hundred miles.

Welcome to LEO.

8. LEO: The Satellite Wars

Altitude: 280 to 1,200 miles away

This altitude — 280 to 1,200 miles — is the most hotly contested zone in all of space.

Low Earth Orbit was, for the first fifty years of the space age, mostly empty. The ISS. Some Iridium satellites, some Earth observation platforms and a handful of science projects made up the bulk of the objects in LEO. Total: a few thousand objects.

By the end of 2026, Starlink alone will operate more than fifteen thousand active satellites.

Amazon’s Kuiper is climbing to more than three thousand. The Space Development Agency’s Tranche 1 and Tranche 2 proliferated warfighter architecture is putting hundreds of small satellites into military LEO. China’s Guowang and Qianfan combined for a stated buildout target of over twenty-six thousand. Iridium NEXT provides IoT and messaging. Planet Labs operates the largest commercial EO fleet ever built. AST SpaceMobile is building the first true satellite-to-cellphone constellation.

LEO is the demand engine of the entire space economy. Every layer below this one — launch, ground, manufacturing, components, materials — is being scaled to serve the LEO buildout. When Starlink adds a hundred satellites this week, and next week, and the week after that, the wave propagates all the way back down to the ore.

The single most important economic fact about LEO is that the SpaceX-led launch cost collapse turned it from a physics problem into a manufacturing problem. The bottleneck is no longer the rocket. The bottleneck is the satellite bus, the propulsion module, the phased array, the star tracker, and the rare earth magnet that spins the reaction wheel. LEO sets the tempo for the entire stack. Own the tempo-setter, and you own the derivative.

Key names:

Iridium ($IRDM): the LEO comms incumbent. Their network is now essential infrastructure for aviation, maritime, and DoD. Boring, dependable, quietly compounding.

Planet Labs ($PL): the largest commercial EO constellation ever launched. If you’re an insurance company, a government, or a hedge fund, you’re probably already buying their data.

AST SpaceMobile ($ASTS): direct-to-cellphone from LEO. If it works at scale, category-defining. If it doesn’t, footnote. Binary.

Rocket Lab ($RKLB): building the SpaceX alternative from the launch pad up — launcher, bus, propulsion. Vertically integrated in a way nobody else in the West is.

But if LEO is where the buildout is at full pace, above it sit the layers that were built decades ago and still have to be maintained.

Whether investors notice or not.

9. GEO & MEO: The Legacy Layer

Altitude: 1,200 to 22,000 miles away

The old-space stack sits between roughly one thousand and twenty-two thousand miles above the Earth. It is where the boomer satellites live.

At the top of the range, geostationary orbit is home to the satellites that took forty years to normalize. Weather satellites. Direct broadcast television. Missile-warning platforms — SBIRS and its successor, Next-Gen OPIR — that watch every meter of the Earth’s surface for a hostile launch. Government communications birds. Legacy commercial comsats.

Below that, medium Earth orbit is the home of positioning, navigation, and timing. GPS III and its successor GPS IIIF are being deployed here. So are the allied constellations: Europe’s Galileo, China’s BeiDou, Russia’s declining GLONASS.

GEO revenue is slow-decline. MEO revenue is slow-growth. Neither is where a growth investor will find a big trade. But both are where the most survivable Pentagon assets live, and both are where the “resilient PNT” thesis lives — the argument that GPS has become jamming-vulnerable, spoofing-vulnerable, and single-point-of-failure vulnerable in an era of great-power competition. This isn’t where growth lives — it’s where sovereign resilience gets funded. The Pentagon has begun contracting for redundancy at MEO in ways that will fund a small ecosystem of new suppliers for a decade, and most investors won’t notice the awards until they’re already priced in.

Key names:

Lockheed Martin ($LMT): GPS III and IIIF prime, dominant hardened-comsat provider. The Pentagon can’t do PNT without them.

Northrop Grumman ($NOC): the missile-warning satellite prime. SBIRS, Next-Gen OPIR, and everything after. Sees every hostile launch on Earth before anyone else does.

EchoStar ($SATS): the GEO comsat operator with a diversified book across commercial broadcast and government contracts. Slow-and-steady legacy business.

Viasat ($VSAT): shows up in both ground and orbit. Broad government-contract exposure, hybrid GEO-plus-LEO strategy, and a footprint most competitors can’t match.

Beyond geostationary is the frontier.

A quarter-million miles out, a second economy is being built.

10. The Lunar Economy

Altitude: 250,000 miles away

The moon is the closest thing this decade has to a real second economy.

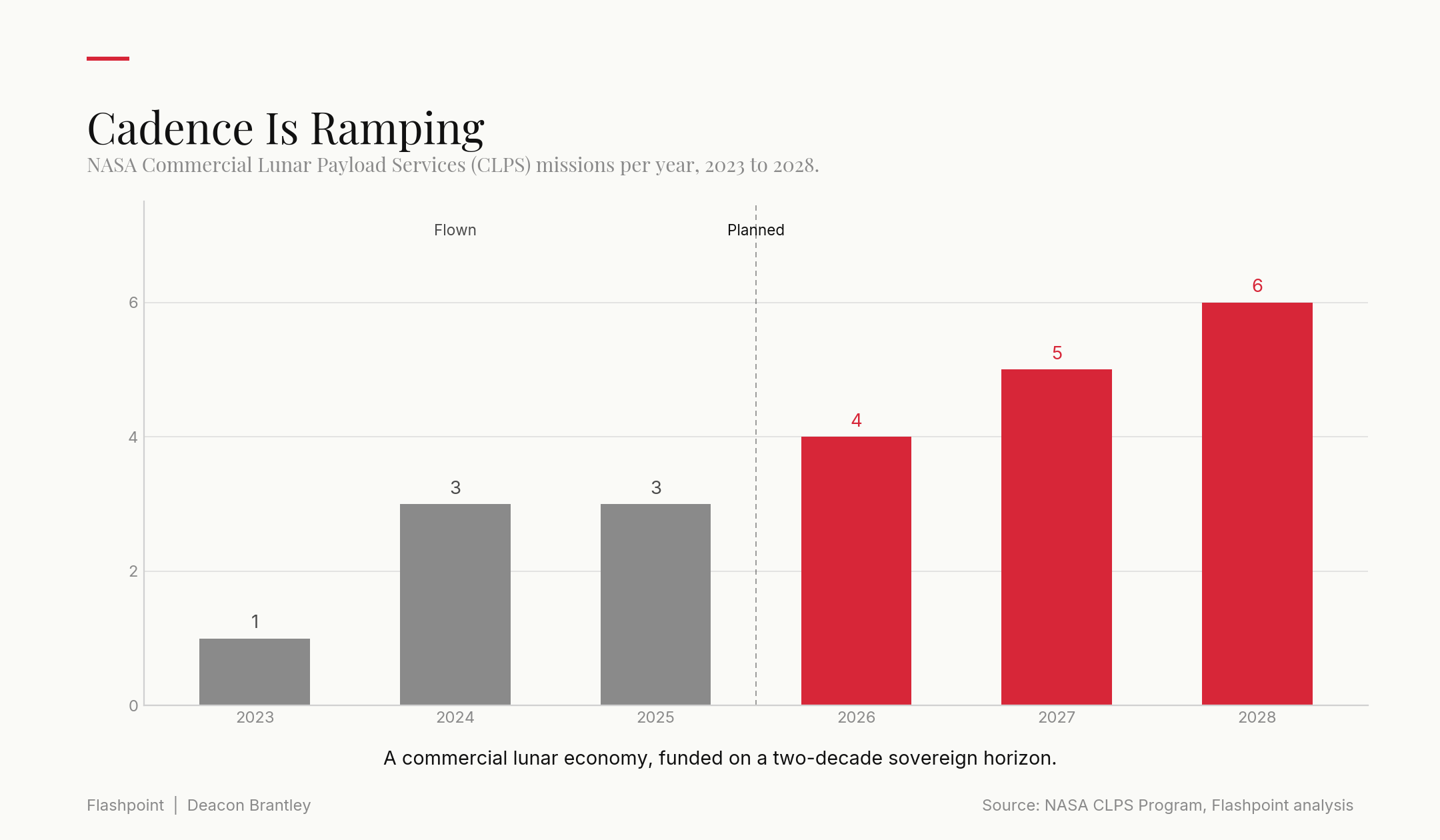

NASA’s Commercial Lunar Payload Services (CLPS) program has already flown its first commercial landers. Intuitive Machines put an American spacecraft on the lunar surface in 2024 — the first since Apollo — and did it as a for-profit contractor. Firefly Aerospace followed in 2025. More missions are on the manifest for 2026 and 2027.

The Artemis program has committed the United States to returning humans to the lunar surface. The contract structure runs through Lockheed (Orion), Boeing (SLS core stage), SpaceX (Human Landing System), and Blue Origin (the secondary lander). Every one of those main contractors depend on the components and materials layers below.

On top of the human program sits the Defense Department’s growing interest in cislunar space domain awareness. If China establishes lunar surface infrastructure this decade — and the state program is credible — then the space between the Earth and the Moon becomes contested territory. That is a Golden Dome extension in all but name. Two sovereign buyers, two different clocks, one infrastructure. Whenever you find that pattern in this piece — NASA on the science side, DoD on the security side — the ecosystem beneath it is being underwritten twice.

Key names:

Intuitive Machines ($LUNR): the first American operator to land on the moon since Apollo. Small-cap, high-beta, and one of the few pure-play lunar names.

Rocket Lab ($RKLB): shows up again. The Photon deep-space bus is what NASA uses for lunar science missions, and the vertical integration means they can build the whole mission end-to-end.

Redwire ($RDW): lunar hardware across Artemis and CLPS. Whatever gets to the surface, some of it was probably built by Redwire.

Kratos Defense ($KTOS): the deep-space comms provider linking the Deep Space Network upgrade to commercial lunar traffic. Quiet essential-infrastructure play.

But the moon is only a proving ground.

The destination that pulls the whole stack is a hundred and forty million miles further.

11. Mars: The Next Frontier

Altitude: 140 million miles away, on average

The commercial architecture that will get to Mars does not exist yet. But it is being built, in full public view, in South Texas.

SpaceX’s Starship program is not a rocket. It is an economic argument. If the vehicle achieves anything close to its stated performance — hundred-ton payload to orbit, full and rapid reusability, refueling in orbit — then the cost of getting mass anywhere in the solar system falls by another order of magnitude. That reprices every layer beneath it in this piece, and it makes the current Mars Sample Return architecture obsolete before it flies.

NASA’s Mars Exploration Program is already being restructured around that assumption. Rocket Lab’s Escapade mission, launched in 2024, was the first commercial-primed interplanetary science mission. It will not be the last.

Mars has no near-term cash flows. What it has is gravitational pull. It is the demand narrative that justifies Starship, and Starship is what reprices launch, and launch is what reprices everything down the stack. Starship’s outcome is binary. If it works, the entire cost structure of the space economy resets downward by a decade. If it doesn’t, launch stays the strategic bottleneck it is today. Either way, it is the single largest binary in the sector.

Key names:

SpaceX ($SPCX): As long as Musk is there, SpaceX will continue dreaming of interplanetary colonization.

Lockheed Martin ($LMT): the prime on JWST’s successors and every outer-planet mission architecture NASA has funded.

Northrop Grumman ($NOC): the JWST builder, and the prime for its successor — the Habitable Worlds Observatory.

L3Harris ($LHX): the Deep Space Network upgrade prime. Their antennas set the throughput ceiling for every deep-space mission humanity ever flies from here.

Boeing ($BA): the SLS and heavy-lift transport prime for sovereign missions beyond LEO. Legacy exposure to every serious government-funded deep-space program.

Beyond Mars is nothing but scientific narrative.

And the antennas that pick up its signals.

12. Deep Space

Altitude: billions of miles away

This is the realm of imagination and possibility.

We are the first generation to look up at Mars and know, with something close to certainty, that human beings will stand on it. Not maybe. Not eventually. In our lifetimes. Every science fiction writer of the last century wrote toward this moment. We're the ones who get to watch it happen.

The James Webb Space Telescope, parked at Earth-Sun Lagrange Point 2 nearly a million miles from home, is the most expensive scientific instrument ever built. Its successor, the Habitable Worlds Observatory, is already funded through early-stage design. NASA’s Europa Clipper is en route to Jupiter’s moon. The Deep Space Network — a set of three enormous radio arrays in California, Spain, and Australia — is being upgraded for the first time in a generation.

This isn’t a cash-flow layer. There are no revenue models here.

What deep space is, is speculation: the ceiling on what the sector believes is possible, and the floor for the deep-space communications infrastructure that everything below relies on.

Every commercial mission that ventures beyond Earth orbit depends on the same DSN dishes. Every Mars lander, every lunar relay, every future asteroid mission is a customer of the same aging network. That network is being rebuilt. The prime contractors on the rebuild — Lockheed, Northrop, L3Harris — are the same names that appeared in the layers below. The stack closes on itself. The vein in Mountain Pass funds the antenna in the Mojave, which catches the signal from a spacecraft fifteen billion miles away.

13. The Trade

We’ve arrived.

A century from now, the historians of this decade won’t write about AI models or election cycles or interest rate paths. They’ll write about the moment humanity stopped treating space as a place to visit and started treating it as a place to build.

We are living through that moment.

Below the moon, an industrial civilization is being wired into orbit — comms, imagery, navigation, defense, eventually habitation. Above it, the first commercial cargo lanes to another world are being cut in a South Texas launch pad. Fifteen billion miles from here, Voyager is still transmitting on twenty-one watts of power, and the country that built it is finally rebuilding the industrial base that made it possible.

Here’s what it comes down to.

Four sovereigns are spending simultaneously on the same industrial base — the U.S. government, the Chinese state, allied constellations, and SpaceX. That base atrophied for thirty years. It cannot be rebuilt in a quarter. Every layer is single-sourced. Most are already repricing on signed order books.

The buyers can’t wait. The suppliers know it.

That’s the trade.

Not one ticker. Not a basket. A shape — from the vein in Mountain Pass to the antenna in the Mojave, repricing all at once, financed by the four largest capital pools on Earth.

If I’m wrong, it’s because Starship failed, Golden Dome got knifed by a new administration, or the Chinese called off their constellation buildout. None of those are impossible. None are what I’m betting on.

If I’m right, this is the trade of the next twenty years. Not because any single stock ten-bags. Because the entire chain reprices at once — and the people who saw the shape early are the ones who benefit while everyone else is still figuring out what the shape is.

The West either owns the orbital infrastructure of the twenty-first century, or it doesn’t.

I know which side I’m on.

Flashpoint | Deacon Brantley — 6 July 2026

Not financial advice. Always do your own research and take care when trading.

Selected sources

Books that shaped the framing: Walter Isaacson, Elon Musk (Simon & Schuster, 2023), and Eric Berger, Reentry (BenBella, 2024).

Government primary: NASA and U.S. Space Force FY2026 budget documents, the January 2025 Golden Dome for America executive order, SDA proliferated warfighter architecture documentation, NASA Commercial LEO Destinations and CLPS program awards, DoD Defense Production Act Title III award records, USGS Mineral Commodity Summaries 2025, and FCC Space Bureau constellation filings.

Industry research: the Satellite Industry Association’s 2025 State of the Satellite Industry Report, BryceTech’s Global Space Economy 2024, IEA’s Global Critical Minerals Outlook 2024, the CSIS Missile Defense Project on hypersonics, and CRS Report R45811.

Company filings: SpaceX’s S-1 and IPO prospectus (June 2026), and 10-K and 10-Q filings for every ticker mentioned above.

Space is one of those topics I never get tired of reading about. Super interesting read, loved it.